To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

New Cigna + Oscar (C+O) small group sales and renewals will not be offered in 2025. At C+O’s request, all plans and rates have been removed from the quote engine. However, you can still quote or renew your C+O groups through December 15, 2024 by contacting us at quotes@claremontcompanies.com or 800.696.4543. Please note: the last day of coverage will be December 14, 2025.

For assistance, please contact our Quotes team at quotes@claremontcompanies.com or 800.696.4543.

Login To PrismTaking advantage of pre-tax benefit plans through a Flexible Spending Account (FSA), Health Reimbursement Arrangement (HRA), or Health Savings Account (HSA) allows your clients to stretch their benefits budget. With access to tax-free funds for qualified medical expenses, these accounts provide a strategic way to maximize savings and better manage healthcare costs. To ensure your clients make the most of their new accounts, here are tips to keep in mind, and reminders of valuable resources from BRI.

Accessing Funds

Checking Your Balance

View the BRI infographic for details.

Know What Expenses Are Eligible

Please review the Plan Highlights to confirm what expenses or expense types are permitted under the plan.

Understanding Your Accounts

Maximize Savings

To learn more, check out the BRI FAQs. These tips and resources will ensure your clients are well informed and prepared to make the most out of their pre-tax benefit plans.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

The IRS has released the 2024 contribution limits for Flexible Spending Accounts (FSAs), Health Savings Accounts (HSAs), commuter benefit plans, and adoption assistance programs. For a summary of the 2024 amounts and plan limits, check out BRI’s overview by plan type and access the IRS official announcements.

*Includes limited purpose FSAs that are restricted to dental and vision care services, which can be used in tandem with HSAs.

To learn more visit Benefit Resource (BRI) and SHRM.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

Offer your clients huge savings on pre-tax or COBRA services for effective dates through January 1, 2024. To qualify, a service agreement must be signed and submitted by September 29, 2023.

To learn more, download the 2023 BRI Fall Incentive Program flyer.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

With more employees returning to the office, the demand for commuter benefits is increasing as commuting to work becomes a regular part of employees’ routines. Offering commuter benefits can provide a valuable incentive for employees, helping them manage the costs associated with their daily commute while promoting their overall well-being.

Commuter benefits provide tax savings of 30% or more, easing the financial burden of daily commuting. By setting aside pre-tax funds, employees can save significantly (as much as $1,500 annually for both mass transit and parking), enhancing their job satisfaction and productivity.

Eligible expenses covered by commuter benefit programs typically include both pre-tax mass transit and pre-tax parking. The Benefit Resource commuter benefit card provides universal access to transit providers throughout the United States ensuring flexibility for employees with extended commutes or multiple modes of transportation.

Flexibility is crucial as commuting patterns change due to staggered work hours, remote work arrangements, or other factors. Programs allowing adjustments based on their schedule and their needs, and rollover of unused balances reduce stress and ensure employees maximize their benefits.

By offering commuter benefits, your clients can help their employees better manage the increasing demands of commuting to work, alleviate financial strain, and enhance their job satisfaction. Learn more.

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

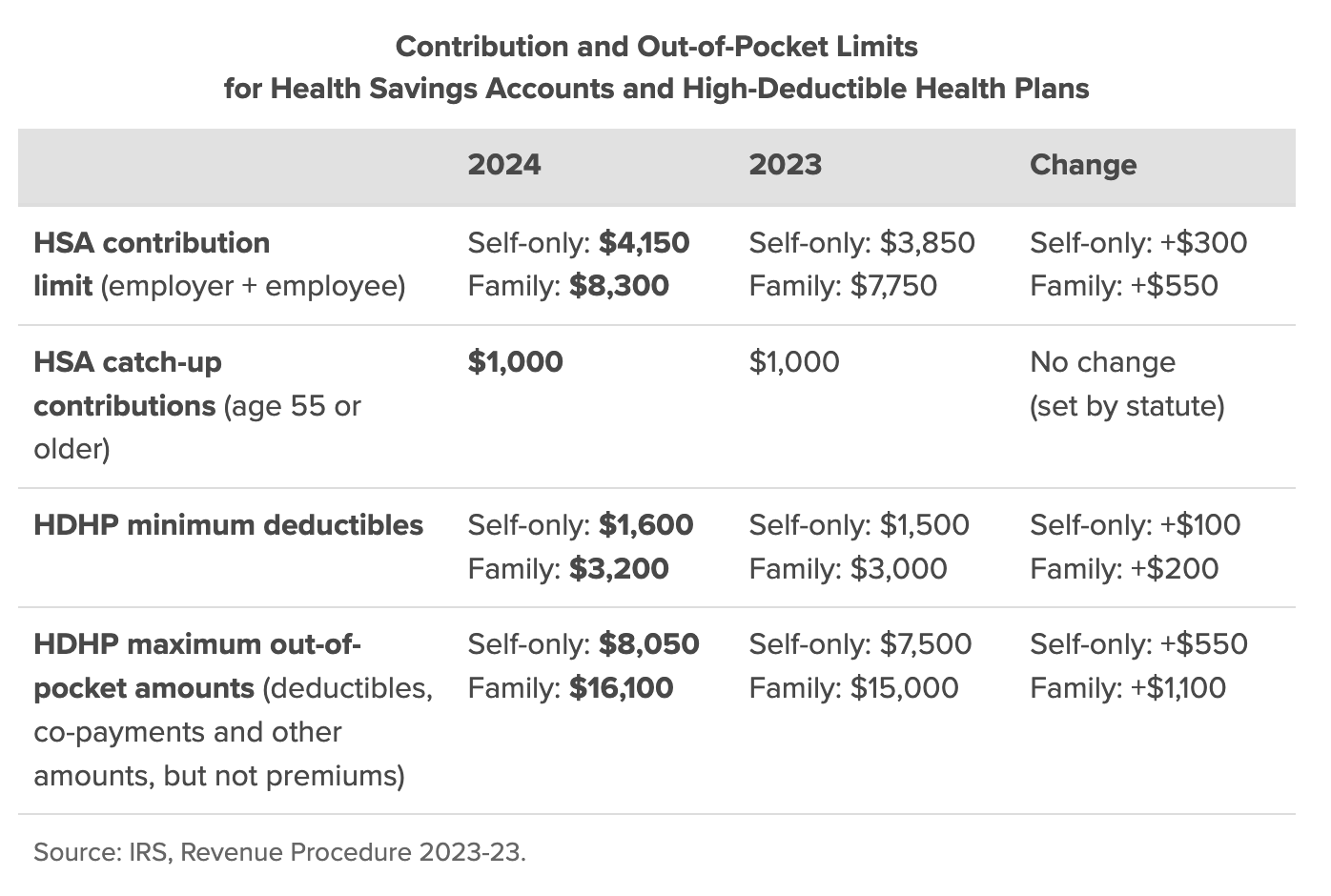

The Internal Revenue Service (IRS) has announced a notable increase in the contribution limits for Health Savings Accounts (HSAs) for 2024, a change that will offer greater flexibility for small businesses, their owners, and their employees.

The annual HSA contribution limit for individuals with self-only High Deductible Health Plan (HDHP) coverage will rise to $4,150, marking a significant increase from the $3,850 limit set in 2023. Similarly, the limit for individuals with family HDHP coverage will increase to $8,300, up from $7,750 in 2023.

In a significant milestone, 2024 marks the first instance where an older married couple, both aged 55 or over, will be allowed to contribute more than $10,000 to their HSAs. This development is made possible by the combination of the increased standard contribution limit and the continuing ability for those aged 55 or older to contribute an extra $1,000 per person. This means that in the last 10 years leading up to retirement, a couple could potentially accumulate more than $100,000 in their HSAs.

The chart below shows a comparison of the 2024 versus the 2023 amounts. Get the details.

Get Help with HSA Administration

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

BRI is offering a new Health Account Outlook Series which will run from February 2023 through April 2023. Through this series they will tackle a variety of topics affecting health accounts including generational and behavior trends, consumer attitudes, how legislation and rules impact your strategy, and some of the hidden challenges (and opportunities) of health accounts.

The Session Will Cover:

Webinar Details

All registered attendees will receive a recording following the live event. Register now!

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

The IRS has announced the annual plan contribution limits for Flexible Spending Accounts (FSA), Health Savings Accounts (HSA), commuter benefit plans, and adoption assistance programs. For a summary of the 2023 inflation-adjusted amounts and plan limits, check out BRI’s overview by plan type and access the IRS official announcements.

*Includes limited purpose FSAs that are restricted to dental and vision care services, which can be used in tandem with HSAs.

To learn more visit Benefit Resource (BRI) and SHRM.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

Join BRI to explore some of the key legislative and regulatory issues affecting employee benefits including:

Webinar Details

All registered attendees will receive a recording following the live event. Register now!

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

Healthcare is a significant investment for your clients, and it’s important that their employees understand coverage options and see value in their benefits. To ensure employees have the proper health coverage and are protected from unexpected expenses, it’s best if they thoroughly review their budget and healthcare needs. The three questions below will help employees prepare for open enrollment before signing up for pre-tax benefits.

Start with looking at how much was spent on healthcare last year. Reviewing spending habits will provide a foundation for the types of financial choices that might be made in the future and how enrolling in a pre-tax account could help.

It may be helpful to place healthcare costs into three categories:

If a spreadsheet or budgeting app was used, consolidate the medical expenses. Then determine, at a high level, what the healthcare expenses were. Make sure to understand how much was paid out of pocket by reviewing exactly what insurance covers annually, and factor that into the plan for healthcare costs. To be safe, add an extra 10-20% to the estimated costs to account for unexpected expenses.

If last year’s medical expenses are unknown, no worries. Review all of the insurance company and healthcare provider receipts and go through bank and credit card statements to identify healthcare costs paid out of pocket last year. Or contact the insurance and healthcare providers for documentation.

According to a report from the Bureau of Labor Statistics, on average, healthcare costs account for about 8% of annual household spending or nearly 7% of pretax income. Even if health insurance covers an expense, the budget for healthcare costs still needs to include health plan premiums.

To determine pre-tax income, look at a recent pay stub before taxes. To calculate after-tax income, look at a bank statement showing paycheck deposits.

These general guidelines will provide a basic understanding of healthcare expenses from the past year and help guide the decisions for open enrollment.

Next, determine if there will be any changes in expenses for the coming year. Specifically, consider out-of-pocket expenses which pre-tax accounts can help pay for.

An out-of-pocket expense is an amount paid after insurance has covered a service.

Determining out-of-pocket expenses can be more difficult. As a starting point, look at current benefits to determine any co-pay or co-insurance amounts. Also factor in the deductible – the amount needed to pay before insurance begins to cover costs. As a general rule, plans with a lower deductible require a higher premium.

For this reason, high deductible health plans (HDHP), also called low-premium plans, have become more popular. HDHPs can also be paired with a Health Savings Account (HSA), which can be a great savings tool for employees.

An HSA lets the employee put money away on a pre-tax basis for eligible healthcare expenses, including certain dental work, eyeglasses, and prescriptions. Contributions can come from the employee, employer, or a relative—anyone who wants to fund the account. Also, the funds roll over from year to year with an HSA, which makes it a great long-term tool for budgeting for medical expenses. Note there is an annual limit for how much they can contribute.

The employee should log into a benefits portal or ask their HR department for their company’s benefits information to find out what these out-of-pocket expenses are.

To determine a dollar amount for out-of-pocket expenses, multiply the co-pay amount by the number of expected healthcare visits. However, keep in mind that some healthcare visits are covered since they are preventative in nature.

For example, if there’s one physical per year, one dental cleaning, and 12 physical therapy visits, most likely only the physical therapy would require a co-pay. If the co-pay is $20, then multiply 20 by 12 for the out-of-pocket costs.

These are expenses for everyday household and personal care items such as adhesive bandages, thermometers, and pain killers.

While these items should be included in the initial review of expenses last year, it’s best to double-check and make sure they’re included.

After accounting for day-to-day healthcare costs, consider unexpected costs for medical emergencies (such as a procedure or medication that is not fully covered by an insurance plan) and create an emergency fund. While the size of the emergency fund will vary depending on lifestyle, monthly costs, income, and dependents, the rule of thumb is to save at least three to six months’ worth of living expenses. A starter emergency fund of $1,000 is recommended.

To budget for healthcare costs effectively, evaluate health insurance options to find the best plan for the employee and their family. For each plan, consider the type of plan (are preferred doctors, hospitals, and pharmacies covered?), as well as the cost of premiums, deductibles, copays, and prescriptions. Health history may also be an important factor when considering different coverage options.

With a healthcare budget in place, employees will be better empowered to make decisions that are good for their health and finances.

To learn more, check out these articles:

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

According to a June 2021 research study from One Medical, 65% of workers would give up bonuses, paid vacation, and flexible hours for better healthcare benefits.

One of the results of the pandemic is that many people now realize the importance of their health and the health of those they’re closest to. Given this shift, it’s no surprise that health and well-being have risen to the top of the priority list for many workers.

However, workers also want more from the companies that are responsible for their benefits. Many aren’t completely satisfied with their healthcare benefits and expect their employers to improve their healthcare options now that well-being is a top priority for them.

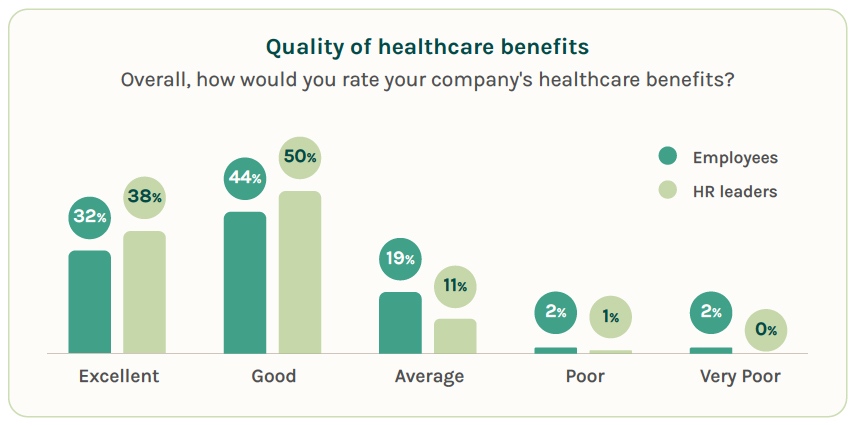

While 85% of HR leaders believe their company is invested in the physical and mental health of its workforce, just 32% of employees rate their healthcare benefits as “excellent” and less than two-thirds believe their company is invested in their physical health (64%) and mental health (63%). Other findings reveal that employees are, in fact, desperate for better healthcare. This should be a strong signal to employers that a change is badly needed – and soon.

The vast majority of workers noted the importance of affordability (89%), ease of using their benefits (89%), top quality and trustworthy providers (87%), fast (86%) and convenient (82%) access to in-person care, a focus on preventive health (85%), and seamless specialty care coordination (82%). While more than half (55%) of employees and HR leaders said their healthcare is too costly and thought companies should cover “more” or “all” of employees’ health care costs.

The study revealed 87% of employees agreed that providing a healthcare offering that is a good value, high-quality, and patient-centered increases job satisfaction, engagement, productivity, retention, recruitment, or the likelihood to recommend the company.

Companies that prioritize the health of their workforce and invest in better healthcare benefits will not only be doing what’s right for their employees, they’ll also be more likely to retain their workers and be better positioned for success in an increasingly competitive marketplace. Download the report to learn more.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.