To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

Why Choose Health Net?

✔ Lowest rates in the market – Affordable options without compromising quality.

✔ Robust PPO network – Competes with major carriers like Anthem and Blue Shield.

✔ Flexible HMO options – Networks to fit nearly every group statewide and every budget.

✔ Simplified underwriting – Only 25% participation required for groups with 5+ enrolling. No DE9C or prior carrier bill needed.

✔ Easy-to-sell benefits – $0 deductible HMO plans + four years of rate stability.

✔ Nationwide coverage – Cigna network access for out-of-state employees + state plurality rules for group qualification.

Start Including Health Net in Your Quotes Today!

Need guidance on networks, plan designs, or have questions? We’re here to help!

Call us at 800.696.4543 | Email us at info@claremontcompanies.com.

Login To Prism

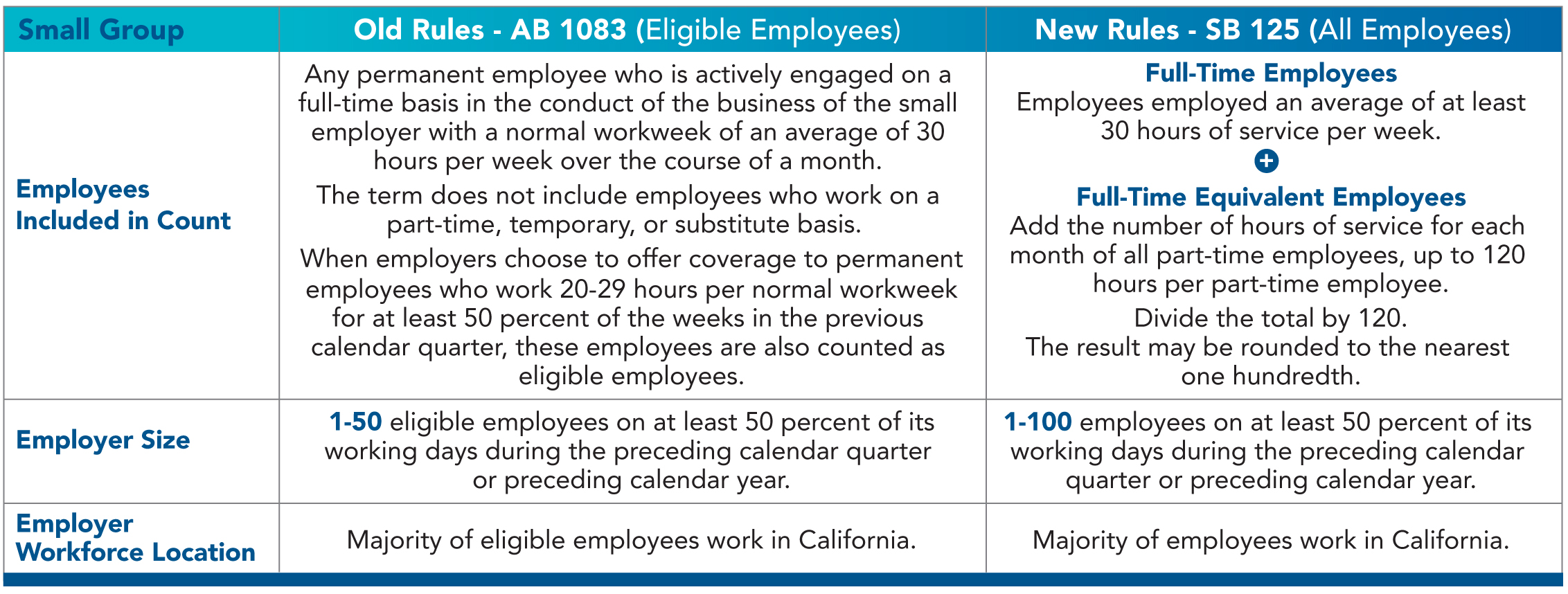

On June 17, the Governor approved Senate Bill (SB) 125. A section of SB 125 revises the definition of small employer for plan years commencing or renewing on or after January 1, 2016. The definition of small employer, for purposes of determining employer eligibility in the small group market, will no longer be based on a count of eligible employees, but shall instead be determined using the method for counting full-time employees and full-time equivalent employees set forth in Section 4980H(c)(2) of the Internal Revenue Code. Quickly see where new rules differ from prior rules by downloading the guide below.

Employer size under Section 4980H(c)(2) of the Internal Revenue Code is determined by taking the sum of the total number of full-time employees and full-time equivalent employees for a calendar month. To be a small employer in California, the result must be at least one, but no more than 100, on at least 50 percent of the preceding calendar quarter or preceding calendar year. The majority of these employees must be employed within California. The requirement that a bona fide employer-employee relationship exists still applies.

A full-time employee is someone employed an average of at least 30 hours of service per week. To calculate full-time equivalent employees, the number of hours of service for a calendar month of all employees who are not full-time are aggregated then divided by 120. No more than 120 hours of service can be credited for any employee who is not full-time. Hours of service includes both working hours and non-working hours for which an employee is paid or entitled to be paid, such as vacation, holiday, illness, incapacity, jury duty, military duty, and leave of absence.

The regulations of Section 4980H(c)(2) specify to include seasonal workers when counting the number of full-time employees and calculating the number of full-time equivalents. A seasonal worker is someone who performs labor or services on a seasonal basis. This employment is only done during certain periods and not throughout the year, such as those who only work during the holidays. Someone who works in agriculture, but performs different activities in different seasons, is considered seasonal, even if they are employed most of the year. A reasonable, good faith interpretation of the term seasonal worker may be applied.

As described above, SB 125 will result in significant changes to the small group market. However, the practical administration of this law has yet to be determined. Stay tuned for updates on this topic.

Questions?

Contact us at 800.696.4543 or info@claremontcompanies.com.