To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

New Cigna + Oscar (C+O) small group sales and renewals will not be offered in 2025. At C+O’s request, all plans and rates have been removed from the quote engine. However, you can still quote or renew your C+O groups through December 15, 2024 by contacting us at quotes@claremontcompanies.com or 800.696.4543. Please note: the last day of coverage will be December 14, 2025.

For assistance, please contact our Quotes team at quotes@claremontcompanies.com or 800.696.4543.

Login To PrismThe San Francisco Office of Labor Standards Enforcement recently released updated Health Care Security Ordinance (HCSO) required health expenditure rates for 2021.

Effective January 1, 2021, the rate per hour will increase:

For-profit employers with fewer than 20 workers and non-profit employers with fewer than 50 workers are exempt.

More information is available on the City of San Francisco HCSO website.

Many have heard of San Francisco’s Healthcare Security Ordinance, which applies to employers based in the city/county of San Francisco, however, you may not be aware of San Francisco’s more costly Healthcare Accountability Ordinance (HCAO), which applies to employers located outside the city/county of San Francisco, but who contract with the city of San Francisco or one of its agencies (such as SF International Airport or the Port of SF).

The HCAO requires employers to offer one of the following to every covered employee (those that work 20 or more hours per week):

The payments in the latter two options are calculated as $4.95 per hour worked (capped at $198 per work week). Union workers are generally exempted as their plans typically meet all the requirements of the HCAO.

Comparing Costs of The Various Options

Compare these choices with the required expenditure under the Healthcare Security Ordinance, which, for each hour worked is $1.89 (companies with 20-99 employees) or $2.83 (100 or more employees).

Conclusions – the HCAO is clearly more costly than the Healthcare Security Ordinance, however, if your client is subject to HCAO, they will have no choice but to comply with it. In that case, it is usually going to be less expensive for them to offer coverage than to pay the hourly rate to the Department of Health or to the employee.

Resources

The San Francisco Office of Labor Standards Enforcement has posted all relevant information on its Healthcare Accountability Ordinance website.

Currently, only employers with 50 or more employees are required to comply with the Paid Parental Leave Ordinance (PPLO), however, that changes on July 1, 2017 when employers with 35 or more employees must comply, and changes again on January 1, 2018 when employers with 20 or more must comply.

The SF PPLO requires employers to supplement compensation that an employee receives through the state’s Paid Family Leave program so that an employee’s compensation equals 100% of their gross weekly wage (up to a cap) during the six-week leave period.

The city of San Francisco’s PPLO web site provides an excellent explanation of the ordinance, how it interacts with the state’s Paid Family Leave program and how to calculate the PPLO benefit. The state’s Paid Family Leave web site is a good resource for employees who think they may qualify.

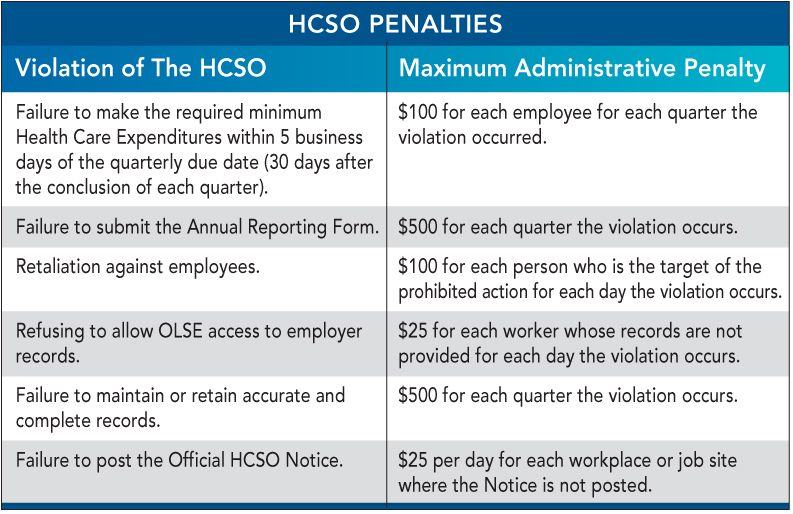

Under the Health Care Security Ordinance (HCSO), all Covered Employers must meet the following obligations:

1. Make the required Health Care Expenditures for all Covered Employees;

2. Maintain records sufficient to establish compliance;

3. Post a HCSO Notice in all workplaces with Covered Employees; and

4. Submit a HCSO Annual Reporting Form to the Office of Labor Standards Enforcement (OLSE) by April 30th of each year.

A Covered Employee may be entitled to Health Care Expenditures for the quarter in which the employee separates from employment based upon the hours payable prior to the separation.

The Covered Employer may satisfy this obligation in two ways. First, the Covered Employer may make the unmade contribution at the time of separation, in which case an accounting of this contribution must be included in the Separation Notice.

Second, the Covered Employer may make a post-separation contribution on its usual schedule, which must be no later than 30 days after the end of the calendar quarter. If the Covered Employer elects to make the final Health Care Expenditure after the separation, the following three criteria must be met:

Health Care Expenditures must be made within 30 days of the end of the preceding calendar quarter.

Revocable expenditures count toward the Employer Spending Requirement provided the employer does not reclaim any part of the expenditure before the earliest of –

*Funds contributed to a Flexible Spending Account do not count as a Health Care Expenditure, because these funds only remain available to the employee for one calendar year. In order to qualify as a Health Care Expenditure, a revocable expenditure cannot be revoked for a minimum of twenty-four months (if the Covered Employee remains employed).

For hours payable on and after January 1, 2017, only irrevocable Health Care Expenditures shall be counted toward the Employer Spending Requirement. In other words, only money actually spent on employee health care can be counted toward compliance with the HCSO. This means that the employer cannot retain or recover any portion of the funds at any time, even if the employee leaves the job or if the business ceases to operate.

Health Reimbursement Arrangements (HRAs), as defined in IRS Publication 969, including excepted benefit HRAs and integrated HRAs, are considered revocable expenditures because the employer has the option to recover any unused funds at some point.

For an allocation of funds to a reimbursement arrangement to be counted toward the spending requirement, the funds must be actually paid over to a third-party trustee who has control over these funds in perpetuity or until the employee exhausts the funds through submitting claims. The employer must have no access to, or control over, these funds and no possibility of ever recovering them.

Examples of Irrevocable Expenditures:

Note: Employers will have until January 30, 2017 to make the required health care expenditures for the fourth quarter of 2016; 20% of expenditures for that quarter will still be permitted to be made revocably.

The City Option allows employers to contribute to the City’s public benefit program on behalf of their employees. Based on the information the employer provides, employees will be provided one of two health benefits:

To be eligible for HSF, the employee must:

a. Live in San Francisco,

b. Be uninsured for at least 90 days,

c. Be age 18 or over, and

d. Not qualify for public health insurance programs (such as Medi-Cal).