To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

New Cigna + Oscar (C+O) small group sales and renewals will not be offered in 2025. At C+O’s request, all plans and rates have been removed from the quote engine. However, you can still quote or renew your C+O groups through December 15, 2024 by contacting us at quotes@claremontcompanies.com or 800.696.4543. Please note: the last day of coverage will be December 14, 2025.

For assistance, please contact our Quotes team at quotes@claremontcompanies.com or 800.696.4543.

Login To PrismEasily help your small business clients and their employees choose the right Health Savings Account (HSA), Health Reimbursement Arrangement (HRA), and Flexible Spending Account (FSA) plan during open enrollment with the Sterling Administration HSA, HRA, and FSA Comparison Guide.

HSA, HRA, and FSA Comparison Guide

Health Savings Account (HSA)

Employers minimize health benefit costs by offering high-deductible health plans (HDHPs) paired with HSAs which require less paperwork than traditional plans, reducing administrative costs. HSAs provide employees added value: unspent funds aren’t forfeited, contributions, growth and withdrawals see triple tax savings, there is investment growth potential, and employees have the option to pay for non-medical expenses from the HSA if needed. Pairing an HDHP with an HSA cuts employer costs while giving employees a valuable, flexible health savings option.

Health Reimbursement Arrangement (HRA)

HRAs encourage employees to be smart healthcare consumers. With an HRA, employers set aside annual funds for employees to use towards health expenses like deductibles and coinsurance not covered by their regular plan. Only employers contribute to these accounts, which offer flexibility in design to meet specific needs. As one of the most adaptable benefits, HRAs are an attractive option for employers to help employees pay healthcare costs.

Flexible Spending Account (FSA)

FSAs are frequently paired with traditional health plans since HDHP enrollment is not required. Traditional plans limit out-of-pocket expenses, allowing employees to better estimate annual medical expenses by calculating projected copays, deductibles, coinsurance, etc. FSAs are intended for spending on healthcare expenses within the plan year, though some plans build in added flexibility

Get Help with HSAs, HRAs, and FSAs

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

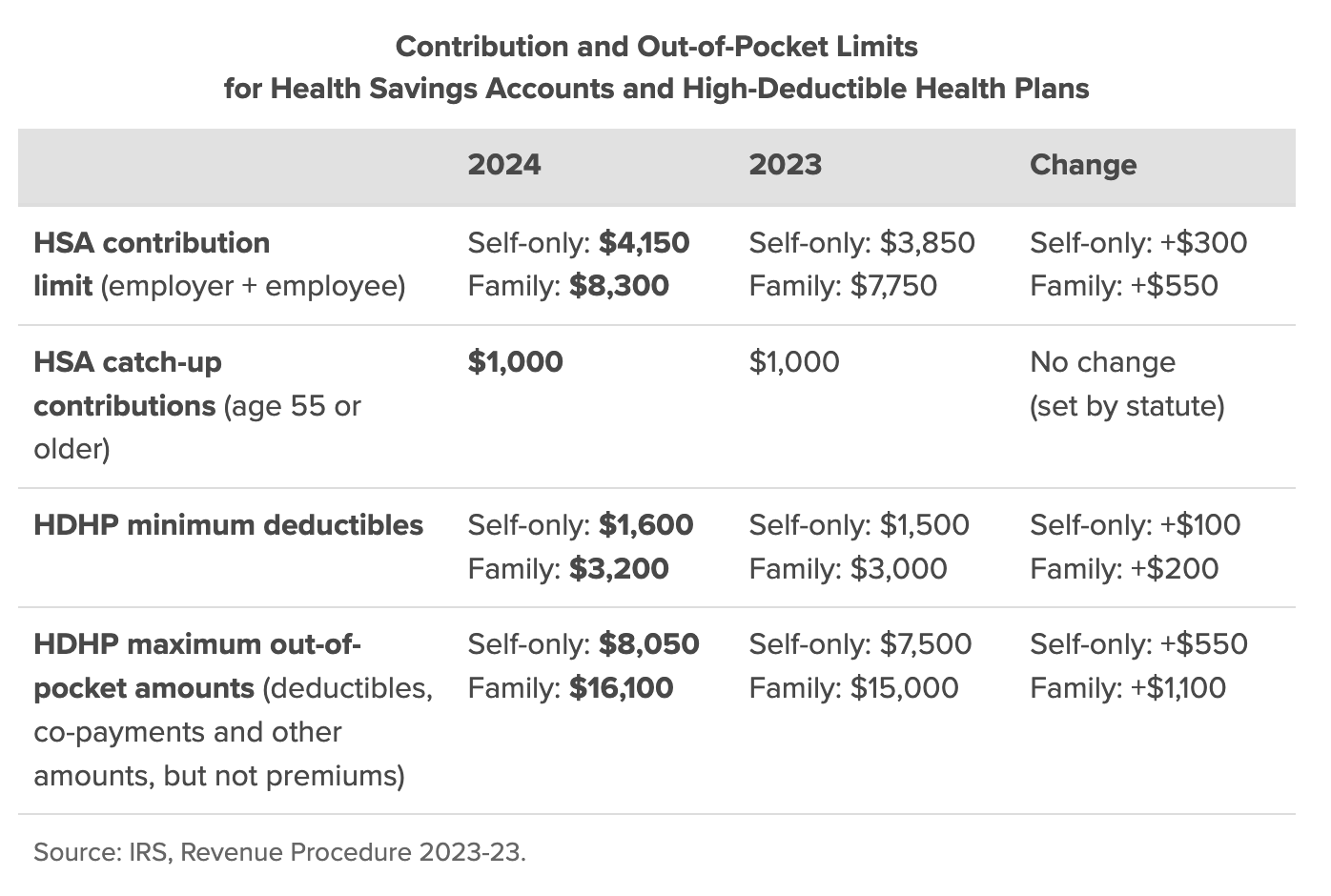

The Internal Revenue Service (IRS) has announced a notable increase in the contribution limits for Health Savings Accounts (HSAs) for 2024, a change that will offer greater flexibility for small businesses, their owners, and their employees.

The annual HSA contribution limit for individuals with self-only High Deductible Health Plan (HDHP) coverage will rise to $4,150, marking a significant increase from the $3,850 limit set in 2023. Similarly, the limit for individuals with family HDHP coverage will increase to $8,300, up from $7,750 in 2023.

In a significant milestone, 2024 marks the first instance where an older married couple, both aged 55 or over, will be allowed to contribute more than $10,000 to their HSAs. This development is made possible by the combination of the increased standard contribution limit and the continuing ability for those aged 55 or older to contribute an extra $1,000 per person. This means that in the last 10 years leading up to retirement, a couple could potentially accumulate more than $100,000 in their HSAs.

The chart below shows a comparison of the 2024 versus the 2023 amounts. Get the details.

Get Help with HSA Administration

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

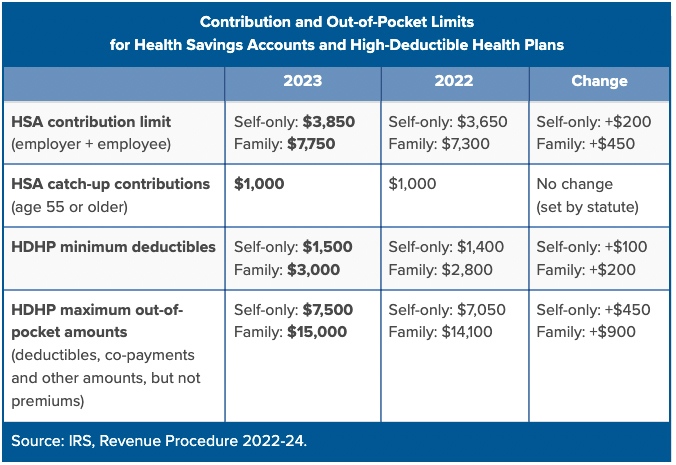

Due to the recent rise in inflation, the IRS announced considerable increases in the 2023 Health Savings Account (HSAs) contribution limits and catch-up contributions; and High Deductible Health Plan (HDHP) minimum deductibles and out-of-pocket amounts.

This early announcement will give employers ample time to plan ahead and communicate with employees about making health care choices before for open enrollment season.

The chart below shows a comparison of the 2023 versus the 2022 amounts. Learn more.

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

The US Department of Labor recently announced that it would ramp up FMLA audits on employers. To ensure your employer groups with 50+ employees are compliant with the FMLA and last year’s significant California Family Rights Act (CFRA) leave expansion, now is a good time for them to review their compliance and administration needs.

The newly launched Sterling Family and Medical Leave Act (FMLA) administration service will:

The FMLA provides eligible employees with up to 12 workweeks of unpaid job-protected leave per year. It also requires covered employers to maintain group health benefits for employees on FMLA leave and offer the same or an equivalent job at the end of their leave.

Employers are eligible and considered a covered employer if they’re a:

Employees are eligible for the FMLA leave if they:

Eligible leaves under the FMLA are:

To learn more, visit Sterling Administration and contact us at 800.696.4543 or info@claremontcompanies.com for assistance enrolling your groups.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

Your clients likely need different benefits offerings to attract and retain employees. Lifestyle Spending Accounts (LSAs) provide employers the opportunity to offer additional benefits that meet the new needs of the workforce.

Funded by employers, LSAs provide employees more choice and pay for lifestyle, health, and wellness benefit options that meet their specific needs. Typical benefits can include:

As an after-tax benefit, an LSA isn’t subject to government reporting requirements, contribution limits, limits on types of disbursements, or categories of employee eligibility. Employer contributions are tax-deductible and employers can decide how often funds are distributed into the account and what types of purchases are considered eligible.

Help your clients incentivize current employees, recruit new employees, and be positioned for success in this challenging environment by offering employees extended benefits to promote their physical, mental, emotional and financial wellness.

To learn more, check out the Sterling flyer and contact us at 800.696.4543 or info@claremontcompanies.com for assistance enrolling your groups in a Lifestyle Spending Account.

Questions?

Contact The Answer Team at 800.696.4543 or info@claremontcompanies.com.

Get The Latest News with Text Messaging!

Your success is important to us, and we’re actively working on new solutions to support you throughout the year. To get the latest news via text messaging in the future, simply provide your cell phone number here.

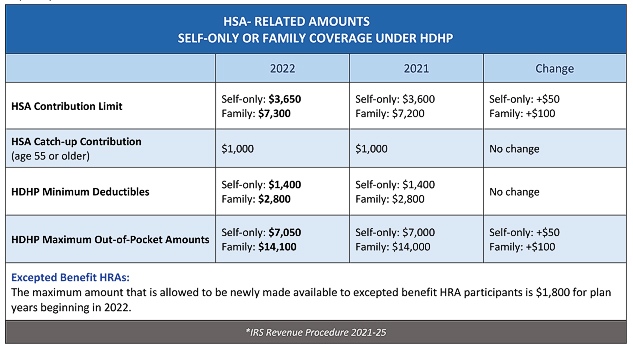

The IRS announced* 2022 inflation-adjusted amounts for Health Savings Accounts (HSAs), HSA-qualified High Deductible Health Plans (HDHPs), and accepted benefit Health Reimbursement Arrangements (HRAs).

The 2022 HSA contribution limits and catch-up contributions, and HDHP minimum deductibles and out-of-pocket amounts are listed in the chart below.

To learn what is eligible with your FSA and HSA plans, check out Sterling Administration’s partner – the HSA Store and FSA Store. It’s an easy-to-use online shopping platform that offers 24/7 chat and online help.

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Help your clients make the most of their accounts with the following tips and reminders.

Accountholders can make contributions to their 2020 plans until tax day 2021. View the video to learn how.

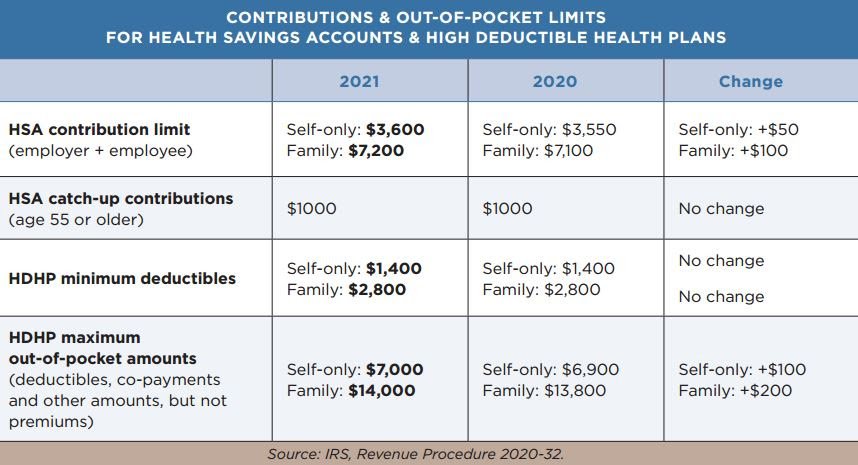

2021 HSA and High Deductible Health Plans (HDHP) Contributions and Out-of-Pocket Limits

Sterling’s Year-End Statement will show you how much is left to spend in your account and your deadlines for spending and reimbursement. To access your Year-End Statement, log in to your FSA account and view “Statements” then select “Year-End Statements.” Click “Run Statement” to generate a report showing any remaining funds left to spend for 2020, and any associated deadlines for associated spending and reimbursement.

The statement may include information on Rollover, Grace Period, or Run-Out Period. Below are the Rollover, Grace Period, and Run-Out-Period definitions.

Rollover

If your plan has a rollover, you may move up to $550 of unused FSA funds to the following plan year. The rollover doesn’t affect the following plan year’s maximum contribution amount.

Grace Period

If your FSA plan has a grace period, you have up to two-and-a-half months at the end of your plan year to spend unused FSA funds and incur new FSA eligible expenses. For example: If you had a December 31 FSA year deadline, your grace period would allow you to use your FSA funds through March 15.

Run-Out Period

If your FSA plan has a run-out period, you have an extended period of time at the end of the FSA plan year to submit receipts for reimbursement. You can only get reimbursed for claims incurred during the previous FSA plan year. The run-out period varies with each plan.

For more FSA information, visit the Sterling Administration website.

Take the guesswork out of what is eligible with your FSA and HSA plans with Sterling Administration’s partner – the HSA Store and FSA Store. It’s an easy-to-use online shopping platform that offers 24/7 chat and online help.

Use these valuable coupons when shopping.

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Help your clients and their employees understand the CARES Act changes to Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs), and Health Reimbursement Arrangements (HRAs) with this recap from Sterling Administration.

What is the HSA Contribution Deadline?

The IRS has confirmed that account holders can make contributions to HSAs for the 2019 plan year up to the new filing deadline of July 15, 2020. The IRS states that contributions to an HSA may be made at any time during the year or by the due date for filing that year’s tax returns. This rule applies to the new federal income tax filing deadline for 2020, which the IRS extended in response to the COVID-19 crisis.

Does my HSA Cover COVID-19 Testing and Treatment?

The IRS (Notice 2020-15 on March 11, 2020) allows high-deductible health plans (HDHPs) to cover testing and treatment for COVID-19 without a deductible. Coronavirus testing and treatment are considered qualified medical expenses under an HDHP, and people can use HSA funds to pay for it. Due to the COVID-19 national health emergency, Notice 2020-15 also applies to HDHPs that would otherwise be disqualified under Internal Revenue Code section 223(c)(2)(A). In other words, HDHPs that provide additional health benefits covering Coronavirus testing and treatment, and HDHPs with a deductible that falls below the minimum requirement are also subject to the Notice.

Does the CARES Act Expand the List of Reimbursable Expenses through an HSA? (Over-the-Counter (OTC) Drugs and Menstrual Care Products)

Yes. The CARES Act states that consumers can purchase OTC drugs and medicines (including menstrual products) with funds from an HSA, FSA, or HRA. Consumers may also receive reimbursement for OTC purchases through those accounts. This provision is effective for purchases and reimbursements of expenses incurred after December 31, 2019. No expiration date.

What Has Changed Regarding Telehealth?

The CARES Act states that “telehealth and other remote care services” below the deductible will be permitted in an HSA-compatible HDHP. This provision is effective immediately and will expire on December 31, 2021.

Does the CARES Act Expand the List of Reimbursable Expenses through an FSA? (Over-the-Counter (OTC) Drugs and Menstrual Care Products)

Yes. The CARES Act states that consumers can purchase OTC drugs and medicines (including menstrual products) with funds from their HSA, FSA, or HRA. Consumers may also receive reimbursement for OTC purchases through those accounts. This provision is effective for purchases and reimbursements of expenses incurred after December 31, 2019. No expiration date.

Can Dependent Care FSA Participants Who Have Lost Preschool and Childcare Services Due to Facility Closures Reduce Their DCA Elections or Terminate Altogether?

Yes. Participants can reduce or terminate their dependent care account elections under these circumstances, as their childcare needs have changed. However, account holders are advised to keep in mind that they may not need to change or revoke their plan elections, even if they are not incurring any new dependent care expenses. Account-holders may be able to claim their full plan year elections once the shelter-in-place orders cease, as childcare expenses can often reach the $5,000 annual contribution limit within 2-5 months.

Does the CARES Act Expand the List of Reimbursable Expenses Through an HRA? (Over-the-Counter (OTC) Drugs and Menstrual Care Products)

Maybe. It depends on how the employer’s specific HRA is set up. Reimbursable expense rules under an HRA plan vary from employer to employer, so your HRA plan documents will need to be reviewed.

The CARES Act states that consumers can purchase OTC drugs and medicines (including menstrual products) with funds from their HSA, FSA, or HRA. Consumers may also receive reimbursement for OTC purchases through those accounts. This provision is effective for purchases and reimbursements of expenses incurred after December 31, 2019. No expiration date.

Take the guesswork out of what is eligible with your FSA and HSA plans with Sterling Administration’s partner – the HSA Store and FSA Store. It’s an easy-to-use online shopping platform that offers 24/7 chat and online help.

Use these valuable coupons when shopping.

Questions?

Contact your Claremont team at 800.696.4543 or info@claremontcompanies.com.

Get Industry news and exclusive updates in

your inbox, weekly.