To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

Why Choose Health Net?

✔ Lowest rates in the market – Affordable options without compromising quality.

✔ Robust PPO network – Competes with major carriers like Anthem and Blue Shield.

✔ Flexible HMO options – Networks to fit nearly every group statewide and every budget.

✔ Simplified underwriting – Only 25% participation required for groups with 5+ enrolling. No DE9C or prior carrier bill needed.

✔ Easy-to-sell benefits – $0 deductible HMO plans + four years of rate stability.

✔ Nationwide coverage – Cigna network access for out-of-state employees + state plurality rules for group qualification.

Start Including Health Net in Your Quotes Today!

Need guidance on networks, plan designs, or have questions? We’re here to help!

Call us at 800.696.4543 | Email us at info@claremontcompanies.com.

Login To PrismUnderstand the San Francisco Health Care Security Ordinance (HCSO) obligations covered employers are required to meet. Visit sfgov.org for more information and resources. View additional FAQ topics.

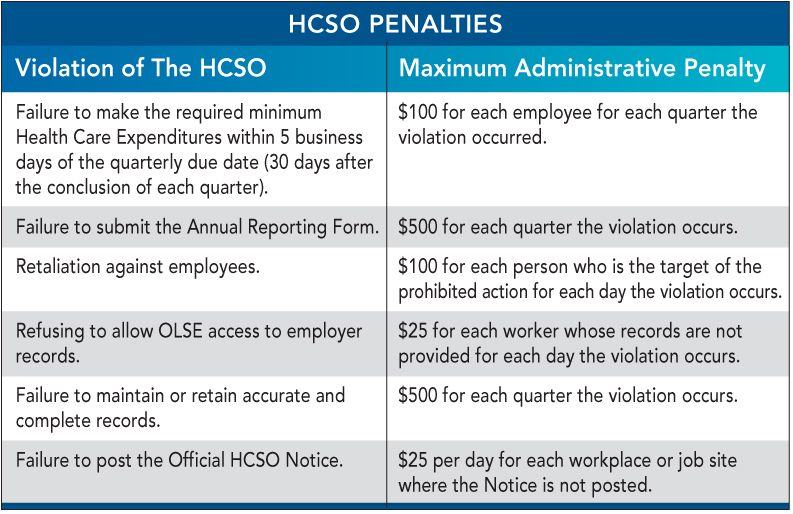

Penalties

PenaltiesWhat are the penalties for violations of the HCSO?

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Making the Required ExpenditureCan an employer allocate Health Care Expenditures for employees then recover any unused funds?

For hours payable on and after January 1, 2017, only irrevocable Health Care Expenditures shall be counted toward the Employer Spending Requirement. In other words, only money actually spent on employee health care can be counted toward compliance with the HCSO. This means that the employer cannot retain or recover any portion of the funds at any time, even if the employee leaves the job or if the business ceases to operate.

Health Reimbursement Arrangements (HRAs), as defined in IRS Publication 969, including excepted benefit HRAs and integrated HRAs, are considered revocable expenditures because the employer has the option to recover any unused funds at some point.

For an allocation of funds to a reimbursement arrangement to be counted toward the spending requirement, the funds must be actually paid over to a third-party trustee who has control over these funds in perpetuity or until the employee exhausts the funds through submitting claims. The employer must have no access to, or control over, these funds and no possibility of ever recovering them.

Examples of Irrevocable Expenditures:

Note: Employers will have until January 30, 2017 to make the required health care expenditures for the fourth quarter of 2016; 20% of expenditures for that quarter will still be permitted to be made revocably.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What are some examples of Health Care Expenditures that meet the requirements of the HCSO?

Payments made directly or indirectly for workers’ compensation or Medicare benefits do not qualify as Health Care Expenditures. Increasing hourly wages, or otherwise giving employees extra money in their paychecks, also do not qualify as a Health Care Expenditure.

An employer may choose more than one option to satisfy its obligations. An employer may, for example, pay for health insurance for its full-time employees while making contributions to the City Option for its part-time employees.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

When do Health Care Expenditures have to be made?

Health Care Expenditures must be made within 30 days of the end of the preceding calendar quarter.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

It depends. The premiums that a Covered Employer pays for medical insurance for its Covered Employees count toward its required Health Care Expenditures, so if that amount meets the minimum required expenditure under the HCSO, the Covered Employer will have no further obligations.

However, if the monthly premium paid by the employer does not meet the minimum expenditure amount, it must make up the shortfall. The employer could choose a health insurance plan that provides more comprehensive benefits; increase its contribution towards the health care premiums while decreasing the portion paid by the employee; or add dental and vision benefits. The employer could also complement the existing plan with a health spending or medical reimbursement account; make payments to the City Option; or make other expenditures that qualify as Health Care Expenditures according to the HCSO.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

A Covered Employer that provides uniform health care coverage (i.e., an HMO or PPO) to some or all of its Covered Employees will be deemed to comply with the spending requirement of the HCSO as to those employees if the average hourly expenditure rate per employee meets or exceeds the expenditure rate required under the HCSO. If the Covered Employer’s expenditure rate fails to meet or exceed the minimum expenditure rate, the employer must spend the difference (or shortfall) within 30 days of the end of the calendar quarter.

Employers shall calculate the average hourly expenditure rate by (a) dividing the total monthly premium paid for all employees covered by the uniform plan by the total number of employees covered by that plan, then (b) dividing that number by 172 hours paid (hours paid per employee is capped at 172 hours in a single month).

The option of averaging expenditures is limited to plans with a uniform design, i.e., the plans must have a uniform benefit design offered to all employees (same co-pay requirements, out-of-pocket maximums, deductibles, coverage tiers, eligibility criteria). An employer that offers an HMO and a PPO may average hourly expenditures for all of the employees covered by the HMO, and calculate a separate average hourly expenditure for those covered by the PPO. Similarly, an employer that offers two HMO options may not average the expenditures between the two HMOs unless the benefit design for both HMOs is exactly the same.

The employer has the option of including only Covered Employees in this calculation, or including all employees participating in the uniform plan, provided that all such employees receive the same health coverage or product.

Amounts paid for dependent coverage may be counted towards the minimum Health Care Expenditure required under the HCSO. Accordingly, contributions for employees with dependents can be averaged with contributions for employees without dependents. However, if differences in the employer’s contribution levels are based on other criteria, i.e., number of hours worked, status as union/nonunion, salary, waiting periods, or work site/location, the expenditures cannot be averaged.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered Employees who already have health care benefits through another employer may voluntarily waive their right to Health Care Expenditures under the HCSO by signing the OLSE’s Employee Voluntary Waiver Form. An employer will not be required to make Health Care Expenditures for employees that choose to sign this form. If an employee who is receiving health care benefits from another employer chooses not to sign the waiver, the employer must make the minimum Health Care Expenditures for that employee.

Keep in mind that the waiver will not be valid unless the health care benefits are provided either by another employer of the Covered Employee or by the employer of that Covered Employee’s spouse, domestic partner, parent, or guardian. If a Covered Employee has health care benefits that are not provided by another employer (i. e., the employee is purchasing it themselves or receiving Medi-Cal), the employee may not sign a waiver and the employer is still required to make the minimum Health Care Expenditures for that employee.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What if employees choose not to participate in the health plan offered?

A Covered Employer that establishes or maintains a health insurance program that requires contributions by a Covered Employee must do more than offer the Covered Employee an opportunity to participate in such a program. If the employee declines to participate in such a program, the employer must satisfy its Employer Spending Requirement in some other manner.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What do my employees receive if I contribute to the City Option on their behalf?

The City Option allows employers to contribute to the City’s public benefit program on behalf of their employees. Based on the information the employer provides, employees will be provided one of two health benefits:

To be eligible for HSF, the employee must:

a. Live in San Francisco,

b. Be uninsured for at least 90 days,

c. Be age 18 or over, and

d. Not qualify for public health insurance programs (such as Medi-Cal).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Revocable expenditures count toward the Employer Spending Requirement provided the employer does not reclaim any part of the expenditure before the earliest of –

*Funds contributed to a Flexible Spending Account do not count as a Health Care Expenditure, because these funds only remain available to the employee for one calendar year. In order to qualify as a Health Care Expenditure, a revocable expenditure cannot be revoked for a minimum of twenty-four months (if the Covered Employee remains employed).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

A Covered Employee may be entitled to Health Care Expenditures for the quarter in which the employee separates from employment based upon the hours payable prior to the separation.

The Covered Employer may satisfy this obligation in two ways. First, the Covered Employer may make the unmade contribution at the time of separation, in which case an accounting of this contribution must be included in the Separation Notice.

Second, the Covered Employer may make a post-separation contribution on its usual schedule, which must be no later than 30 days after the end of the calendar quarter. If the Covered Employer elects to make the final Health Care Expenditure after the separation, the following three criteria must be met:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

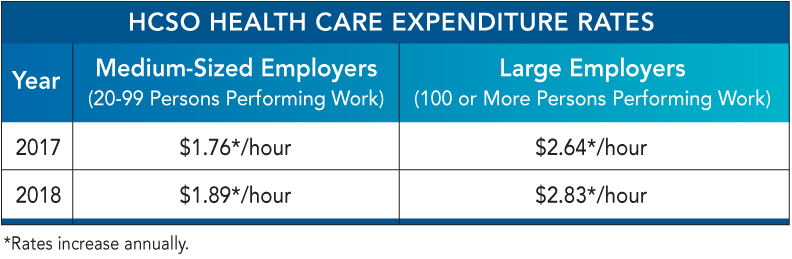

Calculating the Required ExpenditureThe San Francisco Office of Labor Standards Enforcement recently released updated Health Care Security Ordinance (HCSO) required health expenditure rates for 2021.

Effective January 1, 2021, the rate per hour will increase:

For-profit employers with fewer than 20 workers and non-profit employers with fewer than 50 workers are exempt.

More information is available on the City of San Francisco HCSO website.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How much is a Covered Employer required to spend on health care for its Covered Employees?

The minimum Health Care Expenditure for each Covered Employee is determined quarterly by multiplying the total number of hours payable to the employee in the quarter by the applicable Health Care Expenditure rate.

Hours payable includes both the hours for which a person is paid wages for work performed within San Francisco and the hours for which a person is entitled to be paid wages, including, but not limited to, paid vacation, paid time off, and paid sick leave, but not exceeding 172 hours in a single month. Hours payable in a quarter refers to when the payment is earned, rather than when it is actually paid out to the employee.

The employer must make minimum Health Care Expenditures to or on behalf of each Covered Employee. Payments to or on behalf of one Covered Employee that exceed the required minimum Health Care Expenditure for that employee will not be considered in determining whether an employer has met its total required minimum Health Care Expenditures for all employees. There is an exception for employers that provide uniform coverage.

Note that “hours payable” is the figure used to calculate the expenditure required for each Covered Employee, but “hours worked” is used to determine whether an employee is covered by the HCSO.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No. Under the HCSO, hours payable includes only those hours during which the employee is working within the geographic boundaries of the City and County of San Francisco.

For Covered Employees who perform some work outside of San Francisco, hours payable that are not hours actually worked (e.g., paid vacation, paid time off, and paid sick leave) should be calculated on a pro rata basis.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

For employees who are not exempt from the overtime provisions of the federal Fair Labor Standards Act (FLSA) and California law, the Health Care Expenditures are calculated based on all hours worked, including overtime hours worked. Keep in mind that hours payable for each employee is capped at 172 hours per month.

For employees who are exempt from the overtime provisions of the FLSA and California law, the minimum Health Care Expenditures should be calculated based upon a 40-hour work week, capped at 172 hours per month, unless there is evidence that the exempt employee’s regular work week is less than 40 hours. In instances where there is evidence that the exempt employee’s regular work week is less than 40 hours, that figure shall be used in calculating the minimum Health Care Expenditures.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered EmployeesAn employee is covered by the HCSO if s/he works for a Covered Employer and:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are owners considered Covered Employees under the HCSO?

Although owners who perform work for compensation must be counted for the purpose of determining employer size, owners are not considered Covered Employees because they are not entitled to payment of the minimum wage. Thus, the business is not required to make Health Care Expenditures to or on behalf of the owner(s).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes, employees can voluntarily waive their right to have their employers make Health Care Expenditures for their benefit if the employee is receiving health care benefits through another employer. Coverage purchased by the employee for him or herself or that the employee is receiving through Medi-Cal or a county health program, is not benefits received through another employer.

The employee must sign the OLSE Employee Voluntary Waiver Form. If the employee fails to state on the form that s/he is receiving benefits through another employer, or leaves that section of the waiver form blank, the waiver form is not valid. The waiver is valid for one year or until revoked by the employee. Employees cannot waive their rights retroactively.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What if the number of hours that an employee works in San Francisco changes over the quarter?

An employee who regularly works eight or more hours per week in San Francisco is covered by the HCSO. For example: an employee who regularly works one eight-hour day per week for the month of January is a covered employee for that month, even if she does not work during the last two months of the quarter.

For employees whose work hours in San Francisco fluctuate, the employer may average the employee’s hours over the 13 weeks in the quarter. Covered Employers are only required to make Health Care Expenditures during those quarters in which the employee works an average of eight or more hours per week in San Francisco.

For an employee who is terminated before the end of the quarter, the employer would calculate the average by dividing the total number of hours worked during that quarter by the number of weeks employed during that quarter.

Note that “hours worked” is relevant to determining whether an employee is covered by the HCSO, but “hours payable” is the figure used to calculate the minimum expenditure for each Covered Employee.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered EmployersWhich employers are “Covered Employers”?

An employer is covered by the HCSO for any calendar quarter if it meets the following three conditions, regardless if it’s located outside of San Francisco:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Who should be counted in determining employer size?

All persons performing work for compensation* for the employer should be counted (not just Covered Employees). This includes:

*Compensation includes money, benefits, or in-kind compensation, such as room and board, etc.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How is employer size determined if the number of persons performing work changes from week to week?

For businesses employing a fluctuating number of persons during a quarter (13 weeks), employer size is based on the weekly average number of persons performing work for compensation during that quarter.

For example: a business that employs 5 persons during the first 6 weeks of the quarter and 20 persons during the last 7 weeks of the quarter would not be covered by the HCSO because it has employed an average of only 13 persons per week during that quarter:

[(5 persons/week x 6 weeks) + (20 persons/week x 7 weeks)]/13 weeks = 13 persons/week.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What if an employer owns and operates three unrelated businesses?

Businesses that are a “controlled group of corporations” are considered to be a single employer under the HCSO, and all employees of each entity would be counted to determine the size of the employer. If the businesses are incorporated and not members of a “controlled group of corporations” then each is considered a separate business, and the employees of each separate entity will be counted to determine the size of each employer.

Employees of businesses that are not incorporated are counted as working for one employer if the businesses are under common control. For purposes of the HCSO, “under common control” means either (a) one person (individual, estate, or trust) has at least an 80 percent ownership interest in each of the businesses, or (b) the same two to five persons hold more than a 50 percent ownership interest in each of the businesses.

Note that while some corporations may be excluded from the “controlled group of corporations” analysis for income tax purposes, they are not excluded for purposes of the HCSO. It’s best to seek the advice of legal and/or tax counsel to determine controlled group or common control status.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Both the client and the temporary staffing agency, professional employer organization (PEO), or similar entity may be considered a Covered Employer under the HCSO, and each Covered Employer shall have an obligation to ensure that the Employer Spending Requirement has been met. Under California law, a person or entity “employs” a worker if the person or entity: (1) exercises control over the worker’s wages, hours or working conditions, (2) permits the worker to work, or (3) engages the worker (i.e., creates a common law employment relationship).

If a temp agency or PEO performs any of these functions, then that entity is considered a “joint employer,” along with the client for whom the employee performs the work. If there is a joint employment relationship, both entities are responsible for the required Health Care Expenditures. Either entity may make the expenditures, but both can be held liable if the expenditures are not made.

The Health Care Expenditure rate is determined by the size of the larger employer. For example: if a temp agency has 200 employees and the employer at the work site has only 30, the Health Care Expenditure rate for large employers applies.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What obligations are Covered Employers required to meet?

Under the Health Care Security Ordinance (HCSO), all Covered Employers must meet the following obligations:

1. Make the required Health Care Expenditures for all Covered Employees;

2. Maintain records sufficient to establish compliance;

3. Post a HCSO Notice in all workplaces with Covered Employees; and

4. Submit a HCSO Annual Reporting Form to the Office of Labor Standards Enforcement (OLSE) by April 30th of each year.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If you have any questions that we haven't covered yet, we'd love to hear from you. Please click the button below and complete the form. A member of our team will be in touch.

Not finding what you're looking for? Ask a question.

The answers provided are a best interpretation of the information available as of the date posted. The answers are for informational purposes and should not be construed as tax or legal advice.