To access the carrier product and rate information provided by PRISM, check the box below indicating you have read and agree to the license agreement. A button will then appear to access PRISM.

This site uses cookies to track your agreement option. If the terms of the license agreement change or if you clear the cookies from your browser, this page will appear once again during the PRISM login process.

New Cigna + Oscar (C+O) small group sales and renewals will not be offered in 2025. At C+O’s request, all plans and rates have been removed from the quote engine. However, you can still quote or renew your C+O groups through December 15, 2024 by contacting us at quotes@claremontcompanies.com or 800.696.4543. Please note: the last day of coverage will be December 14, 2025.

For assistance, please contact our Quotes team at quotes@claremontcompanies.com or 800.696.4543.

Login To PrismQuickly get a comprehensive overview of Covered California. To find out more about the requirements and unique advantages of Covered California for Small Business, visit our carrier section. View additional FAQ topics.

Agent Agreement

Agent AgreementUse the certified agent’s name, NOT the agency name.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Standard Agreement (Std 213) Contractor Section – Do I use my information or the agency’s?

Use the certified agent’s name and signature and it is OK to use the agency’s address.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Use the certified agent’s name.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

List the agency’s FEIN.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If the agency is to be paid, put the agency’s FEIN.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If the agency is to be paid, the agency should fill out the form and the agency’s authorized payee representative should sign it.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

For those agents who want their commissions to go to an agency, they should put the agency’s FEIN.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Has the agent contract been approved or is it still in draft?

The agent agreement has been approved.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

It is acceptable to submit the declarations page from the agency’s policy as evidence of the agent’s coverage, provided that the agency’s policy does actually cover the agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will the E&O policy need to be in the agent’s name or the agency’s name?

It is acceptable to submit the declarations page from the agency’s policy as evidence of the agent’s coverage, provided that the agency’s policy does actually cover the agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Agent Appointments & CommissionsYes, the applicant can send a letter to Covered California designating their agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the commission on Covered California for Small Business plans?

Covered California for Small Business commissions are paid by Covered California. See commission schedule: https://www.claremontcompanies.com/wp-content/uploads/2015/12/CCSB-2016-Agent-Commission.pdf

Certified Insurance Agents must be appointed by Covered California to receive commissions. Agents do not need to secure appointments with each of the carriers in Covered California for Small Business. Agents will be appointed under the Covered California for Small Business Master Agent Agreement and agents will then have sub-appointments with all participating Covered California for Small Business carriers. The Certified Insurance Agent Agreement includes full vesting language with familiar terms. Agents can be assured that business sold during the year is secured under the agreed-upon commission rate.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will agents be compensated for Medi-Cal enrollments?

Certified Insurance Agents (CIAs) receive $58 for each approved Medi-Cal application when:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How will commission splitting be handled?

Certified Insurance Agents are permitted to split or share commissions provided the other agent is also a Certified Insurance Agent authorized to sell through Covered California. The Covered California for Small Business system does not automatically allow for commission splits but agents can make their own split arrangements until such a feature is made available in Covered California for Small Business. In the individual marketplace, since commissions will be paid by each health insurance company how commissions will be split will depend on the health insurance company’s policies and procedures.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are agents compensated for renewals?

Individual Marketplace – Commissions are set by each carrier in the exchange.

Covered California for Small Business – Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Individual Marketplace – Since commissions will be paid by each health insurance company it would depend on the health insurance company’s policies and procedures. However, each agent must be certified with Covered California to transact business with Covered California.

Covered California for Small Business – Each agent must be certified with Covered California to be appointed by Covered California. Agents do not need to secure appointments with each of the carriers in Covered California for Small Business. Agents will be appointed under the Covered California for Small Business Master Agent Agreement and agents will then have sub-appointments with all participating Covered California for Small Business carriers.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the commission on Covered CA individual plans?

Commissions are paid by each health insurance company according to the Agent’s active commission schedule at the time of enrollment. Certified Insurance Agents must be directly appointed by each of the health insurance companies in Covered California to receive commissions from the health insurance company. The commission rate is the same rate as non-exchange business.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are commissions based on pre-subsidy/credit premium?

Commissions are based on the gross premium and not the net premium.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

There will be a field in the application to designate the agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Notice of Coverage Options Available Through The MarketplaceYes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

PaymentsWill EFT be available during enrollment?

Individual and Family – All payments should be made payable to the selected health plan. Covered California health plans accept payments via personal check, money order, or re-loadable credit, debit and prepaid cards that contain a Visa, Mastercard or American Express symbol. Some Covered California health plans are planning to include other payment options including cash, delivered in-person to a designated payment facility, or Electronic Funds Transfer (EFT)/Automated Clearing House (ACH) transactions. See the chart on page 13 in the Covered California Plan Options participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Which carriers will accept EFT?

See the chart on page 13 in the Covered California Plan Options participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

In order for coverage to start, payment must be received in full by the Covered California health plan that the consumer selects. Hence, if the consumer remits payment between the 16th and the last day of the month, the effective date is the first day of the second following month.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What are Automated Clearing House (ACH) transactions?

It’s a mechanism by which banks are able to transfer money directly from one account to another, i.e. it’s a direct withdrawal from a checking account.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

To whom will Covered California for Small Business premiums be payable?

Covered California for Small Business premiums will be payable to Covered California. Covered California will invoice and collect both initial and monthly premiums from employers and provide payment to the appropriate health plans on behalf of the small business.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

In order for coverage to start, payment must be received in full by the Covered California health plan that the consumer selects.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

PlansAre plan changes permitted by Covered California for Small Business after coverage has started?

Yes. Plan changes are permitted under the following conditions:

This policy applies to both new and renewing CCSB groups.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is pediatric dental an essential health benefit?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are all the plans within a metal tier priced the same?

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What coverage is available for out-of-state employees through Covered California for Small Business?

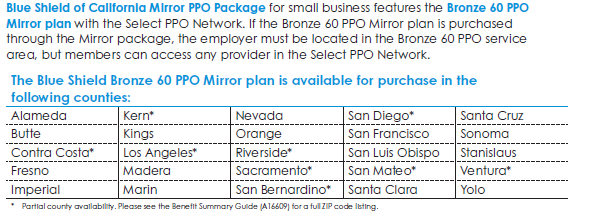

The Blue Shield Bronze PPO 60 plan, with out-of-state coverage through the Blue Card, is available to out-of-state (OOS) employees IF the employer is located in the service area where the plan is offered. Below is the list of counties and/or partial counties where the Blue Shield Bronze PPO is offered.

Normally, employers can only offer two tiers of coverage (Silver and Gold, for example), however, if an employer located in one of the above service areas needs to accommodate OOS employees, Covered California for Small Business (CCSB) will permit the employer to offer the Blue Shield Bronze PPO 60 to OOS members. If the employer is not located in one of the above service areas, then other coverage would need to be considered for these employees. For instance, the employer can opt to offer the eligible OOS employee coverage through the SHOP in that employee’s primary out-of-state worksite.

Note: CCSB had sold plans from Health Net that provided coverage to OOS members, however, in April 2016 Health Net announced that they would no longer cover OOS members. For groups that have existing OOS members on the Health Net plan, they can stay on the plan until the group comes up for renewal. For groups that did not have existing OOS members, they would not be able to add any OOS members after April 2016 so other coverage would need to be considered.

At the group’s renewal, the OOS members do have the option to move to the Blue Shield Bronze PPO 60 plan IF the employer is located in one of the service areas where the plan is offered (see above).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will there be more carriers later on?

Other carriers are welcome to bid to be in the Exchange in 2016.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The “Cadillac Tax” is an excise tax on high-cost health plans. Starting in 2020 an excise tax of 40% will be assessed on the cost of coverage for health plans that exceed a certain annual limit ($10,200 for individual coverage and $27,500 for self and spouse or family coverage).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is pediatric vision embedded in Covered California plans?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Consumers may want to purchase outside of the Exchange for more options. There may be plans outside of the Exchange that have richer benefits or better meet the consumer’s needs. However, any plans in Covered California that are also offered outside of Covered California have to have the same benefits and premiums.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

It depends on their plans out-of-state benefits.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Out-of-pocket costs are the consumers’ expenses for medical care that aren’t reimbursed by insurance. Out-of-pocket costs include deductibles, co-insurance and co-payments for covered services plus all costs for services that aren’t covered.

The out-of-pocket maximum is the most consumers pay during a policy period (usually one year) before their health insurance or plan starts to pay 100% for covered essential health benefits. This limit must include deductibles, coinsurance, copayments, or similar charges and any other expenditure required of an individual which is a qualified medical expense for the essential health benefits. This limit does not have to count premiums, balance billing amounts for non-network providers and other out-of-network cost-sharing, or spending for non-essential health benefits.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the waiting period for grandfathered plans?

On Friday, August 15, 2014, the Governor signed into law Senate Bill (SB) 1034, which prohibits a health benefit plan for group or individual coverage from imposing a waiting or affiliation period before coverage becomes effective.

The intent of SB 1034 is to prohibit a health care service plan or health insurer offering group coverage from imposing a separate waiting or affiliation period in addition to any waiting period imposed by an employer for a group health plan on an otherwise eligible employee or dependent. Furthermore, the intent of SB 1034 is to permit a health care service plan or health insurer offering group coverage to administer a waiting period imposed by a plan sponsor in accordance with the provisions of the Affordable Care Act (ACA). Hence, an employer may impose a waiting period, however it must comply with the ACA, which prohibits waiting periods that exceed 90 days.

SB 1034 will be effective January 1, 2015, however, carriers may choose to incorporate this change prior to the effective date. This applies to non-grandfathered and grandfathered plans.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Does Covered California cover dental?

All individual health insurance plans sold through the Covered California exchange will now include pediatric dental benefits for members younger than 19. Additionally, Covered California is offering new family dental plans to consumers who enroll in health insurance coverage in 2015.

The optional stand-alone family dental plans, which offer coverage for adults, will not be available at the beginning of open enrollment, which starts Nov. 15, but are planned to be added in early 2015. Covered California will offer both dental health maintenance organization (DHMO) and dental preferred provider organization (DPPO) plans, giving consumers a choice in the type of plan that will work best for them. There is no financial assistance available for the optional adult dental benefits.

There is no requirement to enroll children in a family dental plan. The family dental plan is optional and is primarily intended to offer affordable dental coverage to adults that was not available in 2014. Families should consider that adding their children to a family dental plan will result in an extra cost for the same dental services they already receive in their standard health insurance plan. The most likely reason to enroll a child in the family dental plan is if a dental provider they prefer for their child is not offered through their embedded coverage.

Below is a list of the pediatric dental coverage embedded with Covered California’s individual health insurance plans.

| Health Insurance Plan Selected | Pediatric Dental Coverage Embedded into Health Insurance Plan |

| Anthem Blue Cross of California | Anthem Blue Cross |

| Blue Shield of California | Blue Shield of California |

| Chinese Community Health Plan | Delta Dental of California |

| Health Net | Dental Benefit Providers |

| Kaiser Permanente | Delta Dental of California |

| L.A. Care Health Plan | Liberty Dental Plan |

| Molina Healthcare | California Dental Network |

| Sharp Health Plan | Access Dental Plan |

| Valley Health Plan | Liberty Dental Plan |

| Western Health Advantage | Premier Access |

Family dental plans are offered from the companies listed below.

| Optional Family Dental Plans |

| Access Dental Plan |

| Anthem Blue Cross |

| Blue Shield of California |

| Delta Dental of California |

| Dental Health Services |

| Premier Access |

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered California plans are organized into categories of coverage, called metal tiers,

based on actuarial value. The idea is to make it easier for consumers to compare coverage

options and tradeoffs. More information on metal tiers can be found on pages 8 and 9 of the Covered CA Plan options participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are provider networks driven by metal levels?

No. The metal tiers (Platinum, Gold, Silver, Bronze) are determined by the Actuarial Value of the plan, which is independent of the provider network.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes, carriers are all applying similar small group definition rules regarding both “non spouse W-2s” (sometimes referred to as “common law employee”) and 1099s. Check with the individual carriers for their exact rules.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Do all counties in California have Covered California plans?

Covered California (individual exchange and Covered California for Small Business) is available in all counties. Not every plan is available in each county.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How can I identify if my client is enrolled in a grandfathered plan?

Carriers are required to notify consumers with these policies that they have a grandfathered plan and disclose if they are grandfathered in all materials describing plan benefits.

If in doubt, contact the carrier.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What are the eligibility requirements for catastrophic plans?

To be eligible for a catastrophic plan/ minimum coverage plan, the individual must both:

AND

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

When can you enroll outside of the Marketplace?

A health insurance issuer in the group market must allow an employer to purchase health insurance coverage for a group health plan at any point during the year.

A health insurance issuer in the individual market must allow an individual to purchase health insurance coverage during the initial open enrollment period of Oct. 1, 2013 – March 31, 2014. SB 20, which was signed by the Governor on June 16, 2014-

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is pediatric dental included in the plans in Covered California?

Insurers signed contracts to offer pediatric dental coverage in 2014 in both the Exchange’s individual and small-group employer markets. The contracts offer stand-alone plans for children’s dental coverage in the first year. Because of technical constraints, Covered California is unable to offer bundled pediatric dental plans in 2014. However, Covered California pledged to work toward embedding pediatric dental coverage in its 2015 portfolio of comprehensive medical insurance products in the individual exchange. Only stand-alone pediatric dental will be offered in Covered California for Small Business in 2015.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How will consumers know about the provider networks in Covered California plans?

The health plans that are part of Covered California have online directories available on their websites. These directories will list the doctors and hospitals that are part of the health plan’s network.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The following open enrollment periods apply to health plans and insurers in the individual market:

The first open enrollment period will begin on Oct. 1, 2013 and will end on March 31, 2014.

SB 20, which was signed by the Governor on June 16, 2014-

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

When would a child-only plan be suitable?

A child-only plan would be suitable, for example, in the following situations:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How long can grandfathered plans remain in effect?

As long as the carrier continues to offer it, and the plan continues to meet the grandfather requirements.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Which carriers are participating in Covered California?

Individual and Family Market:

Anthem

Blue Shield

Chinese Community Health Plan

Contra Costa Health Plan

Health Net

Kaiser

L.A. Care Health Plan

Molina Health Care

Sharp

Valley Health Plan

Western Health Advantage

Covered California for Small Business:

Blue Shield

Chinese Community Health Plan

Health Net

Kaiser

Sharp

Western Health Advantage

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can a health plan charge more to a member with health problems (Diabetes, Heart Disease)?

No. In California, only age, family size, location and plan design can be used to determine rates.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can minimum coverage plans/ catastrophic plans be sold to people over 30?

Minimum coverage plans/catastrophic plans can be offered to people under age 30 and to those without affordable coverage options or those eligible for a hardship exemption.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No. Grandfathered plans are those that were in existence on March 23, 2010 and haven’t been changed in ways that substantially cut benefits or increased costs.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Networks may be different inside Covered California. However, any plans in Covered California that are also offered outside of Covered California must have the same benefits and premiums. Check with the individual carriers for their provider networks.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can people still buy direct or will pricing be better with Covered CA?

Any plans in Covered California that are also offered by the carrier outside of Covered California have to have the same benefits and premium rates.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are there any HSA plans for individuals available in Covered California?

There are HSA-qualified high deductible health plans (HDHPs) available in Covered California’s individual exchange. For example, the Blue Shield of California Bronze 60 HSA Plan.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes. Any plans in Covered California that are also offered outside of Covered California have to have the same benefits and premiums.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Must grandfathered plans provide the full suite of mandated preventive benefits at no cost?

Preventive health benefits with no cost-sharing does not apply to grandfathered plans.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are there Evidence of Coverage (EOC) documents on Covered California?

Not yet.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Do people on dialysis qualify for a Covered California plan now?

Health plans are banned from imposing pre-existing condition exclusion on children under age 19. In 2014, the ban on excluding coverage of pre-existing conditions is extended to adults as part of a broader set of 2014 insurance reforms.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will groups be able to change carriers out of open enrollment outside of the Exchange?

In the small group market outside the exchange, employers can cancel coverage at any time and also apply for coverage with another carrier at any time.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No, the private market is also an option.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Where do plans outside of Covered California fit in?

Plans outside of Covered California are part of the range of options available to consumers.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

For what age is the pediatric dental and vision?

Under age 19.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the AV of catastrophic plans?

Catastrophic plans can have actuarial values less than 60%.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Where does a consumer check for drug formularies?

The health plans that are part of Covered California will have online drug formularies available on their websites.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the out-of-pocket max?

The maximum out-of-pocket limit allowed by regulation for health plans (inside and outside of the Exchange) is $6,350 for individuals and $12,700 for a family. Plans may have lower out-of-pocket limits.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

It is our understanding that all individual and family non-grandfathered plans in the private market will be replaced by the carriers with ACA-compliant plans.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How are premium rates based on family composition calculated?

Each family member will be charged based on the premium of their age. However, health plans can only charge for the three eldest children under 21. All children age 21 and older are charged premiums based on their age.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the difference between individual and Covered California for Small Business plans?

Covered California Health Plans in the Individual Marketplace.

Information on Covered California for Small Business plans can be obtained through PRISM, Claremont’s proprietary quoting system for brokers.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will out-of-pocket maximums include copayments for Rx?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

For a catastrophic plan, what constitutes not having affordable coverage for those over 30?

If the individual’s required contribution for coverage for the month exceeds 8% of the individual’s household income, then the individual cannot afford coverage.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If you sign up and change your mind as to company or benefit can you change?

Yearly open enrollments allow for these types of changes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is Essential Community Provider Requirements (Tab 4, slide 19 of 41, in the training binder)?

A Qualified Health Plan (QHP) issuer must have a sufficient number and geographic distribution of essential community providers, where available. Essential community providers are providers that serve predominantly low-income, medically underserved individuals in the QHP’s service area.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is there a catastrophic plan in Covered California for Small Business?

No, catastrophic plans are only offered through the Individual Marketplace.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is included in out-of-pocket costs?

Out-of-pocket cost, also called cost-sharing, refers to the amount the consumer pays for covered services at the time they use them. It usually includes:

• Coinsurance (e.g. 20%)

• Co-payments, or similar charges ( e.g. $45/doctor visit)

• Deductibles

Out-of-pocket costs generally do not include:

• Monthly premiums

• Balance billing amounts for out-of-network doctors and hospitals

• The cost of non-covered services or not medically necessary services

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How can plans with different co-pays be in the same metal level?

Cost-sharing structures could vary from one plan to another, but still achieve the same actuarial value. For example, one plan may have a higher deductible than another, compensating by having a lower coinsurance percentage once the deductible is met in order to achieve the same actuarial value.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What are the rates in Covered California for employees 65 and older?

There is a single age band for adults ages 64 and older. Moreover, rates shall not vary by more than 3 to 1. Rates, however, vary by plan, hence it is best to obtain a quote.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How many plan options are available within the Marketplace?

There are 33 plans in Covered California for Small Business.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are there limited visits for speech, physical therapies?

Health plans can no longer impose annual or lifetime dollar limits on essential health benefits. The list of essential health benefits includes rehabilitative and habilitative services and devises. These include physical, occupational, and other therapies and treatments to help people regain function after an accident or illness (“rehabilitative” services), or to help them maintain (rather than regain) their ability to function on a daily basis (“habilitative” services).

As for limits on visits, there are no limits on Department of Managed Health Care plans, but there can be limits on Department of Insurance plans.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is the premium rate based on the individual’s age at the time of application or approval?

The premium rate is based on the individual’s age as of the effective date.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can you discuss/address the difference between AV and minimum value?

Actuarial value (AV) is the percentage of costs a health plan will cover for a standard population.

Minimum value means the total allowed costs of benefits provided under the plan is no less than 60%. Basically, the plan has to have a 60% AV.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Who determines the pricing regions?

The California legislature in coordination with California regulators.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Rate changes, including carrier rate changes and rate changes due to a birthday, will occur on renewal.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Premium Assistance & Cost Sharing ReductionsWhat is counted in household income?

Household income is the sum of a taxpayer’s modified adjusted gross income (MAGI) plus the aggregate MAGI of all the individuals for whom a taxpayer properly claims a deduction for personal exemption and are required to file a tax return.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are individuals enrolled in retiree coverage eligible for the premium tax credit?

Individuals enrolled in an employer-sponsored plan, including retiree coverage, are not eligible for the premium tax credit, even if the employer plan is unaffordable or fails to provide minimum value. The individual may be eligible for a premium tax credit for another family member who enrolls in Marketplace coverage and is not enrolled in the employer plan

The individual may be eligible for the premium tax credit if the individual declines the coverage from a former employer, such as COBRA or retiree coverage, even if it is affordable and provides minimum value.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can an individual get the premium tax credit subsidy if the individual is eligible for COBRA?

If the individual declines the COBRA coverage, even if it is affordable and provides minimum value, the individual may be eligible for the premium tax credit.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the limit on repayment of excess premium assistance?

If an individual’s income changes, any excess amount that was overpaid in premium assistance would have to be repaid to the federal government as a tax payment. However, there are limits on the excess amounts to repaid and is as follows:

| If Household Income Is: | The Dollar Limit for Single Filers Is: | The Dollar Limit for Joint Filers Is: |

| Less than 200% of the FPL | $300 | $600 |

| At Least 200% of the FPL but less than 300% of the FPL | $750 | $1,500 |

| At Least 300% of the FPL but less than 400% of the FPL | $1,250 | $2,500 |

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What if income lowers and the person doesn’t notify Covered California?

If a tax filing unit’s income changes, and the filer should have received a higher amount, this additional credit would be included in their tax refund for the year. On the other hand, any excess amount that was overpaid in premium credits would have to be repaid to the federal government as a tax payment. However, there are limits on the excess amount to be repaid for those below 400% of the Federal Poverty Level.

Consumers are required to self-report changes in income to Covered California within 30 calendar days from the date of the change. Consumers can report these changes via the online application or by calling the Covered California Service Center.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Why not buy bronze at all times if low income?

Cost-sharing subsidies are only available to individuals enrolled in silver plans. Moreover, premium assistance is available in the other metal tiers. Finally, plans in the other metal levels may better suit the consumer’s needs.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Plans in the other metal levels may better suit the consumer’s needs. For instance, gold and platinum plans will have richer benefits, but bronze plans have lower premiums. Moreover, premium assistance is available in the other metal tiers. Finally, not everyone will qualify for cost-sharing reductions.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

An individual would not be eligible for the cost-sharing reductions if the employer provides minimum essential coverage that is affordable and of minimum value. Affordable means the employee’s portion of the premium, for employee-only coverage, is 9.5% or less of the employee’s income. Minimum value means the plan has at least a 60% actuarial value, i.e. for an average population, it is expected to pay at least 60% of allowed costs.

It is also important to note that the cost-sharing reductions are only available in the silver tier of Covered California’s Individual Marketplace.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If she meets the eligibility requirements. See pages 12-14 in the Eligibility for Individuals and Families participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Household income is the sum of a taxpayer’s modified adjusted gross income (MAGI) plus the aggregate MAGI of all the individuals for whom a taxpayer properly claims a deduction for personal exemption and are required to file a tax return. Hence, if the taxpayer does not claim a deduction for personal exemption for another individual, only the taxpayer’s income will be considered for eligibility for premium assistance.

See example on page 15 in the Eligibility for Individuals and Families participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is there a resource to learn how the premium tax credits are calculated?

See the following:

http://www.fas.org/sgp/crs/misc/R41137.pdf

http://www.cbpp.org/files/QA-on-Premium-Credits.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Does unemployment count as income?

Unemployment compensation is included in the MAGI calculation.

See: http://laborcenter.berkeley.edu/healthcare/MAGI_summary13.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

A household includes individuals for whom a taxpayer claims a deduction for a personal exemption. Hence, the household size would depend on how many individuals are claimed. In this situation, it would be a household size of 3 in the odd years and a household size of 2 in the even years.

See the following link for a more detailed explanation and examples:

http://www.cbpp.org/files/Household-Definitions-Webinar-7Aug13.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Premium tax credits are calculated based on an individual’s “fair share” of premium. “Fair share” increases with income, and ranges from 3.5% of income at 139% of FPL to 9.5% of income at 400% of FPL.

Individuals will pay their “fair share” of premium, or the total premium, whichever is less.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If your daughter is a dependent on your tax return, then your household income will be used to determine her eligibility for subsidy. If she files her own taxes, her own income will be used to determine her eligibility for subsidy. Subsidies are based on current income.

Looking for a primer on how Covered California works for individuals and families, including subsidy eligibility?. Click here for an informative webinar recently hosted by Covered California.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Parents can purchase Covered California plans for their children without purchasing plans for themselves. The child’s eligibility for premium assistance is determined by the household income.

Covered California hosted an agent webinar that includes a primer on how subsidy eligibility works. More information is available here:

https://www.claremontcompanies.com/wp-content/uploads/2013/11/CoveredCA-CustomerRolloverWebinar_11_08_13.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If the person meets the eligibility requirements. See pages 12-14 in the Eligibility for Individuals and Families participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is there a minimum payment after subsidy?

In certain instances, the credit amount may cover the entire premium and the taxpayer pays $1 towards the premium. In other instances, the taxpayer may be required to pay part or all of the premium. The amount of the tax credit will vary from person to person depending on the household income of the taxpayer (and dependents), the premium for the exchange plan in which the taxpayer (and dependents) is (are) enrolled, and other factors.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes. You can find a table of eligibility by FPL here:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Firstly, Covered California recommends that individuals with mixed eligibility situations such as this use the online calculator at www.coveredca.com.

The husband is ineligible for Covered California if he is on Medicare.

In order for either a husband or wife to be eligible for subsidies, they must file taxes jointly. The wife’s eligibility for subsidies will be determined by the household income (MAGI).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Please explain cost sharing reductions.

Cost sharing reductions (CSR) help people with their out-of-pocket costs such as deductibles, coinsurance and copayments. It is only available to people who enroll in in a silver plan. The issuers provide the extra help with out-of-pocket costs by covering more of the costs of covered benefits, hence increasing the actuarial value of a silver plan. As a result, the individual pays lower deductibles, coinsurance, and/or copayments.

There are three levels of savings available to people who qualify for a CSR. The level of savings is based on the family’s income. See table on page 18 in the Eligibility for Individuals and Families participant guide.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Premium tax credits are calculated based on an individual’s “fair share” of premium. “Fair share” increases with income, and ranges from 3.5% of income at 139% of FPL to 9.5% of income at 400% of FPL.

Individuals will pay their “fair share” of premium, or the total premium, whichever is less.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Does someone with income below 138% always qualify for Medi-Cal?

If the individual meets all the eligibility requirements. See pages 8-12 in the Eligibility for Individuals and Families participant guide.

If so, why are they included in Covered California premium assistance tables?

The tables apply to states that did not opt to expand Medicaid, hence Medicaid coverage is limited to those up to 100% of the federal poverty line.

Note: To qualify for Medi-Cal, an individual must meet both financial and non-financial criteria, such as citizenship and immigration requirements. For example, most individuals who are not citizens but are lawfully present in the United States are not eligible for Medicaid for the first five years that they are in the United States. Hence, the individual may be eligible for premium assistance and cost-sharing reductions.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are premium tax credits and cost sharing reductions available outside the exchange?

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

See the table on pages 7-8 in the following link: http://www.fas.org/sgp/crs/misc/R41997.pdf Also see Attachment E on p. 7 of Covered California’s individual application: http://www.coveredca.com/PDFs/paper_application/CA-SingleStreamApp_92MAX.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

When dependent coverage is “offered” in an employer-sponsored plan (regardless of employer contribution to the dependent coverage) subsidy eligibility will be dependent on the affordability of the employee-only share of premium costs and if those costs exceed 9.5% of the employee’s household income. Costs for dependent coverage are not part of the affordability calculation with respect to employer-sponsored coverage. So if the employer’s offer of coverage is affordable according to this measure, neither the employee nor the dependents will be subsidy eligible.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes, an individual can cancel their Grandfathered plan and enroll in Covered California. Subsidy eligibility will be determined by the regular criteria, and not related to any previous enrollment in an (individual) Grandfathered plan.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The employee and family can enroll in a Covered California plan at full cost. If the employer-sponsored coverage is of minimum value, and is affordable to the employee, then the employee will not be eligible for subsidies. If the dependents are eligible for the employer coverage, and the coverage is of minimum value, and is affordable to the employee, then the dependents will not be eligible for subsidies.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If this individual’s parents claim him/her as a tax dependent, then his/her subsidy eligibility will be determined by his/her parent’s household income. If s/he is not claimed as a tax dependent, his/her subsidy eligibility will be determined by his/her own income.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Who is included in a taxpayer’s family, i.e. household size?

A taxpayer’s family (household size) includes individuals for whom a taxpayer claims a deduction for a personal exemption (see IRS code: http://www.gpo.gov/fdsys/pkg/USCODE-2011-title26/pdf/USCODE-2011-title26-subtitleA-chap1-subchapB-partV-sec151.pdf). This may include the taxpayer, the taxpayer’s spouse, and dependents. Dependents include a qualifying child, or a qualifying relative. A qualifying relative is someone (1) who bears a relationship to the taxpayer, such as a father and/or mother; (2) whose gross income for the calendar year in which the taxable year begins is less than the exemption amount; (3) whom the taxpayer provides over one-half of the individual’s support for the calendar year in which the taxable year begins; and (4) who is not a qualifying child of the taxpayer or any other taxpayer. (See IRS code: http://www.gpo.gov/fdsys/pkg/USCODE-2011-title26/pdf/USCODE-2011-title26-subtitleA-chap1-subchapB-partV-sec152.pdf)

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The IRS ensures that any excess amount that was overpaid in premium credits are repaid to the IRS as a tax payment.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can individuals that are lawfully present apply for premium assistance and cost-sharing reductions?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How are cost-sharing reductions administered?

Consumers who get cost-sharing reductions will pay less out-of-pocket when they use health care services.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Households include individuals for whom a taxpayer claims a deduction for a personal exemption even if those individuals are not in need of health insurance.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are assets included in the income calculation?

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is Modified Adjusted Gross Income (MAGI)?

Gross income is total income minus certain exclusions (e.g. public assistance payments, employer contributions to health insurance payments). From gross income, adjusted gross income (AGI) is calculated to reflect a number of deductions, including trade and business deductions, losses from sale of property, and alimony payments. MAGI is defined as AGI plus certain foreign earned income and tax-exempt interest. For premium assistance purposes, the definition of MAGI will include non-taxable Social Security benefits.

See: http://laborcenter.berkeley.edu/healthcare/MAGI_summary13.pdf

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered California uses the consumer-friendly term “premium assistance” in referring to the Advance Payment of the Premium Tax Credit (APTC).

Consumers who are eligible for premium assistance can choose when and how

they want to apply their premium assistance amount.

Consumers have the following options:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is income based on gross or net income?

Income is based on Modified Adjusted Gross Income (MAGI).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What happens if one does not report changes in a timely manner?

It depends on the change. For example, if the individual’s income changes, the individual may no longer be eligible for premium assistance. There will be reconciliation at the end of the year and the consumer may be required to pay back advance premium assistance. Another example is if the individual does not report a special enrollment qualifying event, the individual may not be able to take advantage of the special enrollment period.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Premium assistance or tax credits are paid by the federal government from penalties and taxes that are part of the ACA.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Change in employer-sponsored coverage – for example, the individual’s employer now offers minimum essential coverage that is affordable and of minimum value.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Covered California’s individual marketplace application requires the applicant to include in the application children who live with them as well anyone on their federal income tax return. However, there is a section that asks whether the other individuals on the application aside from the primary applicant are also applying for health insurance. Moreover, there is a section on the application that asks whether the person claiming the dependents is a parent without custody.

As for the determination of the taxpayer’s family, a taxpayer’s family includes individuals for whom a taxpayer claims a deduction for a personal exemption (see IRS code: http://www.gpo.gov/fdsys/pkg/USCODE-2011-title26/pdf/USCODE-2011-title26-subtitleA-chap1-subchapB-partV-sec151.pdf).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is income based on individual income or household income?

Household income is used for determining eligibility for premium assistance and cost-sharing reductions.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If an individual does not pay taxes does that mean they are not eligible for subsidies?

Applicants seeking premium assistance must intend to file taxes or be claimed as a tax dependent in the coverage year. However, if an individual’s household income is less than the applicable filing threshold, their income may be below 138% of the federal poverty line and therefore may be eligible for Medi-Cal.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What if my income changes after I apply?

If information that you put on your application changes during the year, you must report it. Changes in things like address, family size and income can affect whether you qualify for Medi-Cal or qualify to get help paying for your health insurance through Covered California.

If you have Medi-Cal, you must report changes to your local county office within 10 days of the change. If you have health insurance through Covered California, you must report changes within 30 days.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can married couples that file taxes separately apply for premium assistance together?

Married couples must file jointly for the benefit year in which they are applying for coverage in order to apply the premium assistance amount as a credit to their taxes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can an individual employee apply for the cost-sharing reduction under group coverage?

No, premium assistance and cost-sharing reductions are only offered through Covered California’s individual market.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can an applicant take advantage of both cost-sharing reductions and premium assistance?

Premium assistance and cost-sharing reductions are available to individuals whose household income is between 138% and 250% of the federal poverty line (FPL). Only premium assistance is available to individuals whose household income is between 250% and 400% of the federal poverty line (FPL).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No, premium assistance and cost-sharing reductions are only available through Covered California.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

There will be reconciliation at the end of the year and the consumer may be required to pay back advance premium assistance. Hence, it is important to report any income changes to Covered California.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No, cost-sharing subsidies are only available to individuals enrolled in silver plans.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The application processing times are as follows:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Which tax year will the Marketplace use to determine household income?

The taxpayer’s actual household income for the taxable year will be used. Marketplaces will use data from tax filings and Social Security data to verify household income information provided on the application, and in many cases, will also use current wage information that is available electronically. If the data submitted as part of the application cannot be verified using IRS and SSA data, then the information is compared with wage information from employers provided by Equifax. If Equifax does not substantiate the information on the application, the Marketplace will request an explanation or additional documentation to substantiate the applicant’s household income.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Agent ConcernsNo, that’s incorrect. Covered California for Small Business is a health insurance marketplace that offers any California small business (1-100 employees) a choice of quality, affordable health insurance from multiple trusted carriers.

A wide range of California employers benefit from the many advantages offered by Covered California for Small Business. Discover the advantages here.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How does an employer make an Agent-of-Record change in Covered California for Small Business?

The employer group must write a letter to Covered California and state who their current agent is and who they want their new agent to be. The letter should be dated and signed by an employee of the group who is authorized to make the decision. The letter should be mailed to:

Covered California

P.O. Box 7010

Newport Beach, CA 92658

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can enrollment counselors refer leads directly to CIAs?

Certified enrollment counselors can refer business to certified insurance agents, but certified insurance agents cannot share commissions with the certified enrollment counselors.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will there be an agent link to the portal so agents get credit for the sale?

There is no current ability to link an agent’s website with Covered California’s website. However, agents can create a profile on the Covered California website and there will be a field on the enrollment form that allows consumers to select/designate their agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can agents use translators that are not Certified Insurance Agents?

If the translator is using the CALHEERs system to enroll and maintain groups, the translator will need to be a Certified Insurance Agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Anyone using the CALHEERs system to enroll and maintain groups will need to be a Certified Insurance Agent.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Claremont Insurance Services is authorized to represent Covered California for Small Business.

As an authorized Covered California for Small Business general agent, Claremont offers you:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes. To update your profile, simply select ‘Employers’, and de-select ‘Individuals/ Families’ in the ‘Clients served’ section.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

I can’t access my Covered California agent portal. Help!

A number of agents have reported that they can’t access their agent portal. Many of them, it turns out, created two accounts for some reason. There can only be one “certified” account per agent/license #. These agents have been trying to access their clients through a non-certified account. Here’s what to do to check if this is the problem that’s impacting you:

Determine if the account is “certified” by looking at the Certification Status screen. See the screenshot in the link here:

https://www.claremontcompanies.com/wp-content/uploads/2014/01/CoveredCA-Agent-Certification-Status-Screenshot.png

If Certification Status indicates “Certified,” then that’s the account you should use and to avoid confusion you should call the service center (1-877-453-9198) and have the other account deleted.

If Certification Status indicates “Eligible”, as in the screen shot, then that account is not valid, but you shouldn’t delete this “Eligible” account until you have confirmed you have a “certified” account.

If you don’t know the username and password for an account, you will need to call the service center to get the username and get a password reset.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How is the public going to find their closest agent?

Consumers can search for agents according to consumer preferences, e.g. location, language.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the broker of record (BOR) process in Covered California for Small Business?

Covered California uses the term agent of record (AOR). A new agent of record is assigned when Covered California receives a notice in writing from the employer designating the new agent of record. Notices should be sent to Agents@covered.ca.gov.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What slide 17 of the Compliance Standards section of the training manual is explaining is that agents are not allowed to coach the consumer to provide inaccurate information on the application regarding income, residency, immigration status and other eligibility rules.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Who should the agent contact to get pre-approval for marketing materials?

Review and approval of advertising materials should be submitted to Covered California at agents@covered.ca.gov.

Agents should allow at least 10 business days from the date of the request for Covered California to review any materials submitted. When submitting required materials for approval, indicate the following in the subject line: Advertising Approval Request – Agent name and material type. When submitting revised material, indicate so in the body of the email and include the original submission date of the material. Do not bundle multiple materials in the same submission email. Send a separate email for each material. The only exception is translations. Translations may be sent in one email along with the corresponding English version if available.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can we use the Covered California logo on our business cards?

Covered California has developed a Certified Insurance Agent logo to designate insurance agents who have met the requirements established by Covered California. The logo is available to Certified Insurance Agents to use on their websites, business cards, letterhead and other communications materials.

See agent tools: http://hbex.coveredca.com/agents/tools

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the status of the Navigator program?

A request for applications was released on June 30, 2014.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can Certified Insurance Agents take a paper application, then process it online for our clients?

Online applications have been delayed until Fall 2014.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Do certified enrollment counselors have E&O coverage?

No.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the impact of the ACA on the San Francisco Health Care Security Ordinance (SF HCSO)

The City and County of San Francisco recently published FAQs on the HCSO and the Affordable Care Act. Click here:

http://sfgsa.org/index.aspx?page=6306

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Why would consumers need an agent if they can go online and sign-up?

Certified Insurance Agents bring a depth of experience to consumers by:

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

It is best to check with your Errors and Omissions provider for guidance.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Certified Enrollment Counselors only assist consumers in Covered California’s Individual Marketplace.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

CalHEERS is the California Healthcare Eligibility, Enrollment and Retention System. It is a web-based system that streamlines the eligibility and enrollment process for all products and programs available through Covered California.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can an agent take the Covered California 8-hour certification class only and receive CE credit?

Yes. The agent will get CE credit after having taken the 8-hour class. The agent does not need to complete any other steps towards certification in order to receive CE credit for having taken the 8-hour class. The agent will need to follow the usual process: create an account with Covered California and then log into the Learning Management System to sign up for a class.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How much information will Certified Enrollment Counselors need and have access to?

Certified Enrollment Counselors will have information about consumers, health insurance, affordability programs, and Covered California health plans in order to provide in-person assistance to consumers and successfully enroll them in coverage.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Will agents be able to make changes to their Covered California account?

If agents would like to make changes to their Covered California account (the one first established when registering for training), they will be able to so do once all steps in their certification process have been completed. At that time they will be able to modify their agent profile and payment information (to direct payments to their agency rather than themselves).

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

You should report it to Covered California.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How can Covered CA give rate information without being licensed?

Assuming the question pertains to Certified Enrollment Counselors, Certified Enrollment Counselors have been trained and certified to describe available health care options and guide the enrollment process. Certified Enrollment Counselors, however, cannot recommend specific health insurance companies.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Broker of Record or Agent of Record?

Covered California uses the term “agent” rather than “broker.”

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is there a reciprocal agent certification agreement with out-of-state Exchanges?

Currently there is no reciprocal agent certification agreement with out-of-state Exchanges.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

What is the role of your company (Claremont) to an agent like me?

As a General Agent, we provide product information regarding our carriers; assist with running proposals; provide market information; and assist with enrollment, post-sales support, and claims issues.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can individual/family plan transfer from one agent to another using agent of record?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Are there bilingual marketing materials available now?

Yes, marketing materials are available now in English, Spanish, Chinese, and Vietnamese.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How are Certified Enrollment Counselors paid?

Certified Enrollment Counselors have to be affiliated with a Certified Enrollment Entity and the Certified Enrollment Entity is paid $58 for each initial application during open or special enrollment; $58 for each re-enrollment application; and $25 for each annual renewal application.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The funding for the implementation of Covered California is already in place. Hence, the defunding of the ACA has no short-term impact on California’s implementation.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

You would have to abide by the regulatory, Marketplace, and carrier requirements of that state.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

The first agent will remain the agent-of-record until Covered California receives a notice in writing designating a new agent-of-record.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Do agents assist with annual re-certifications or is that done by Covered California?

The role of the agent includes promoting and supporting retention efforts, which includes coverage renewals, eligibility redeterminations, etc.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Is Covered California ready to take appeals?

Yes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Individual Family Eligibility & EnrollmentIf an individual enrolls in COBRA, can the individual switch to Covered California?

If the individual enrolls in COBRA coverage and the special-enrollment period lapses, the individual cannot cancel the COBRA coverage and enroll in a Covered California health plan until 1) the COBRA coverage is exhausted, 2) the individual has a different qualifying life event for special enrollment, or 3) the next annual open-enrollment period.

If the individual stops paying the COBRA premium and loses coverage (or if the employer has agreed to pay for a limited time and the individual does not continue the payments), the individual will not be eligible for special enrollment through Covered California. The individual will only qualify for special enrollment if:

If none of these reasons apply, the individual will have to wait until the next Covered California open-enrollment period to cancel the COBRA plan and sign up for a Covered California health insurance plan, unless there is another qualifying life event for special enrollment. It’s also important to know that if the individual decides to drop or forgo COBRA and enroll in a Covered California plan, the individual cannot go back to COBRA.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

If a couple has no income, can they qualify for Covered California?

If the couple’s household income for the taxable year is below 138% of the federal poverty level, which it probably will be if they have no income, they may be eligible for Medi-Cal if they also meet the other eligibility requirements.

See pages 8-12 in the Eligibility for Individuals and Families participant guide.

If the couple is eligible for Medi-Cal they will not be able to receive premium assistance or a cost-sharing reduction through Covered California. However, they can buy a Covered California plan at full cost.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

Can members of the same family be on different plans and metal tiers?

Yes, however, currently the system will only allow one member of the family to get the premium assistance in advance. The other members of the family would have to receive the premium assistance at the end of the year when filing taxes.

There may be a more recent answer to this question. Contact Claremont for an update.

(View Full Answer)

How can clients find out the status of their individual applications?

See below a link to a Covered California Application Status FAQ: